Key Takeaways

- QuickBooks fits smaller teams that mainly need accounting; dedicated property management software fits growing multifamily operators that need accounting, rent collection, maintenance, portals, and reporting in one workflow.

- The most important QuickBooks setup step is creating separate company files for business operations and managed properties, or reports and owner funds become muddled.

- As portfolios scale, QuickBooks struggles with property management-specific accounting needs, including separate owner payouts, security deposits, repairs, and reporting across many units.

- Property management software adds tenant and owner portals, online rent payments, work orders, lease reminders, screening, listings, custom reports, check printing, and ACH or card collections.

What is the best property management software for your rental properties?

Is QuickBooks rental property accounting a good solution?

Or do you need a dedicated property management software?

It can be confusing—and overwhelming—trying to navigate all the various options out there. The purpose of this guide is to help you solve that problem.

Whether you’re a property manager or landlord, a good piece of software can make managing your properties so much easier.

Fortunately, it’s not quite as confusing as it might seem at first.

In this guide, we’ll help you decide whether QuickBooks or a dedicated property management software solution is best for providing the functionality you need to manage your properties most effectively.

Along the way, we’ll also show you how to get started in QuickBooks, what its strengths and limitations are, and why you might want to choose a dedicated property management software solution instead.

First thing’s first: is QuickBooks suitable for handling your property management accounting needs?

Can You Use QuickBooks for Property Management Accounting?

The short answer: yes, you can use QuickBooks for property management accounting. But... you probably won’t like it very much.

If you have a larger rental property managent business, chances are a more dedicated property management software solution will make your life much easier.

Like any business, you need an accounting system you can count on, whatever form that takes.

It would be beneficial for you to have a way to track accounts payable, receivables, maintenance and repair cost; issue payments to owners; and generally figure out whether you’re profitable or not.

Not to mention, you want everything in order if and when you decide to secure funding.

QuickBooks isn’t the easiest software to use. Sometimes, it can feel like it requires its own specialized college degree to figure out how to do certain things.

However, if you’re just starting and need something that will handle the basic accounting tasks for managing your properties and your personal accounting, QuickBooks could be the right way to go.

If you’re more experienced or are managing a large number of properties, whether you’re part of a team at a property management firm or on your own, chances are you’ll find QuickBooks limiting in what it can do.

We’ll go into detail on why that is later, but for now just know that although QuickBooks might be your comfort accounting tool, it is not designed for property management; it can only handle so much responsibility before leaving you in the dust.

Now, let’s dive into step-by-step instructions for using QuickBooks for essential property management accounting functions, including setting up your property and tenants and recording transactions in QuickBooks.

How to Set Up QuickBooks for Property Management Accounting

Below, the example we’ll use is of a rental property business.

Property owners or managers can use these same steps with slight modifications (or omissions), though, if you’re managing your own properties.

The first and most important thing to get right in QuickBooks is to make sure you set up two separate company files:

- Your business: This is your property management business, where you accept payment for your services, issue payments to owners, etc.

- Your service: This is your rental property management service, including collecting rent payments, accepting security deposits and other fees, paying for maintenance and repairs, and anything else involved in actually managing the properties for your owners.

It’s vital that you keep these two parts of your business separate. Your accounting reports will be muddled if you don’t, and it will be virtually impossible to distill out any valuable insights.

First, let’s set up the company file for your business itself.

How to Set Up Your Property Management Company File in QuickBooks

With this company file, you’ll record all transactions related to running your business on an administrative level:

- Income received from your services

- Payroll

- Expenses such as insurance and utilities

- Assets, such as equipment

Here’s how to get it started:

1. Set up each property owner as a customer

First, let’s set up your clients.

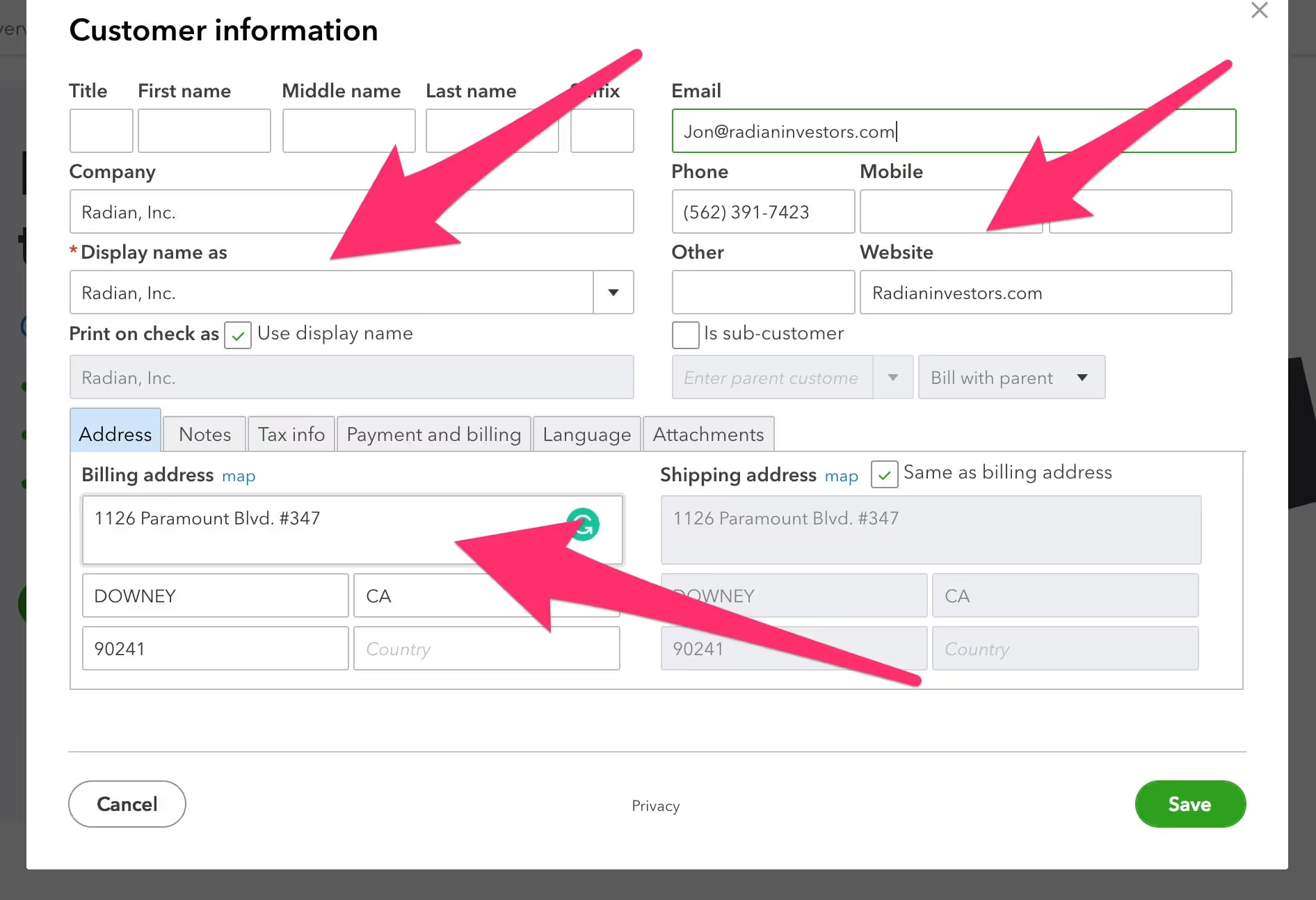

In QuickBooks, click “Add customer:”

Then, plug in all your client’s information:

Click “Save,” then repeat these steps for the rest of your clients.

2. Add your accounts

Now, it’s time to set up the accounts where you’ll track all your accounting activity.

Start by going to your chart of accounts, which you can get to by clicking on the sidebar under “Accounting:”

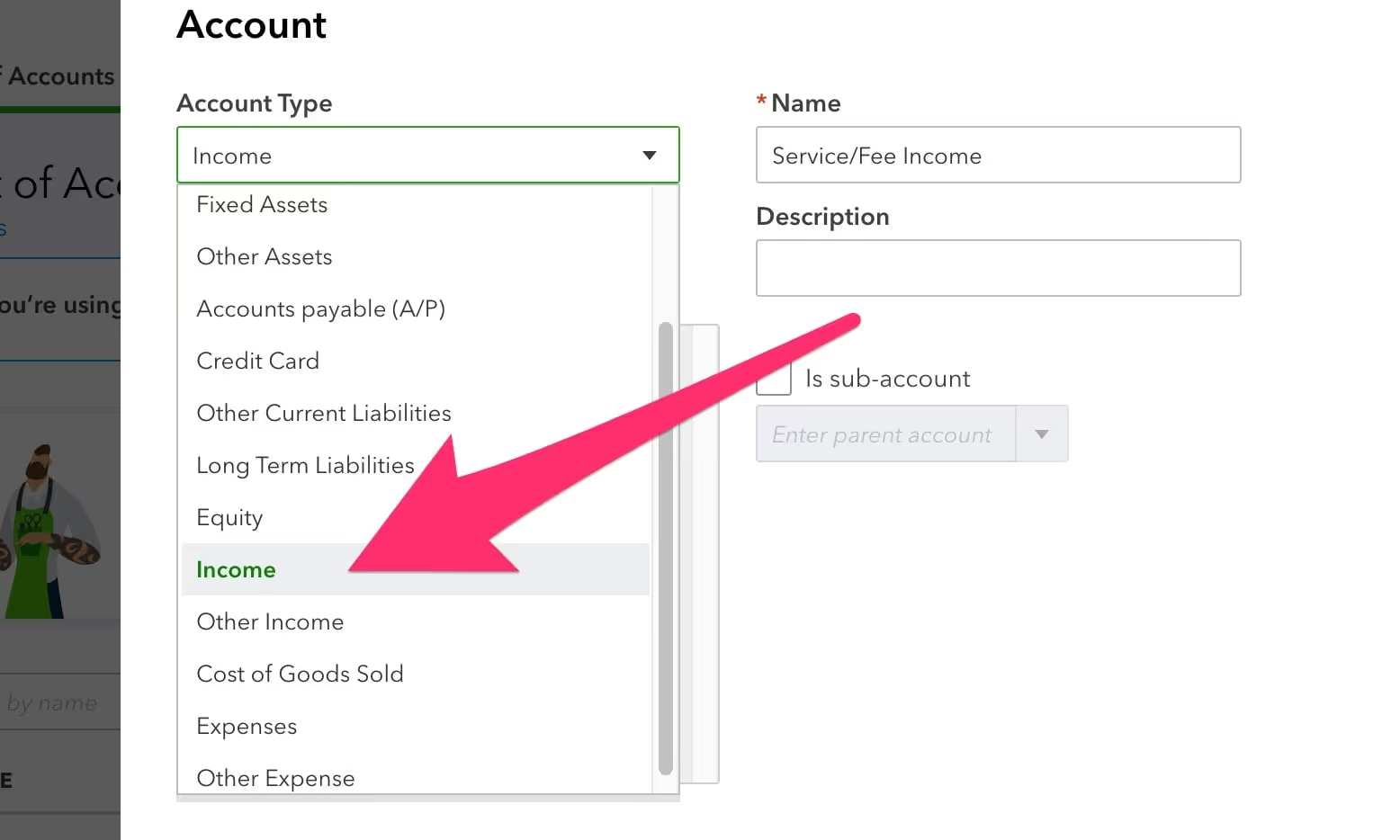

Then, click “New” to create a new account:

Select the proper primary account from your chart of accounts:

QuickBooks will automatically create one for you, but it may not be ideally suited for property management. More on that is discussed here in our Property Management Chart of Accounts guide.

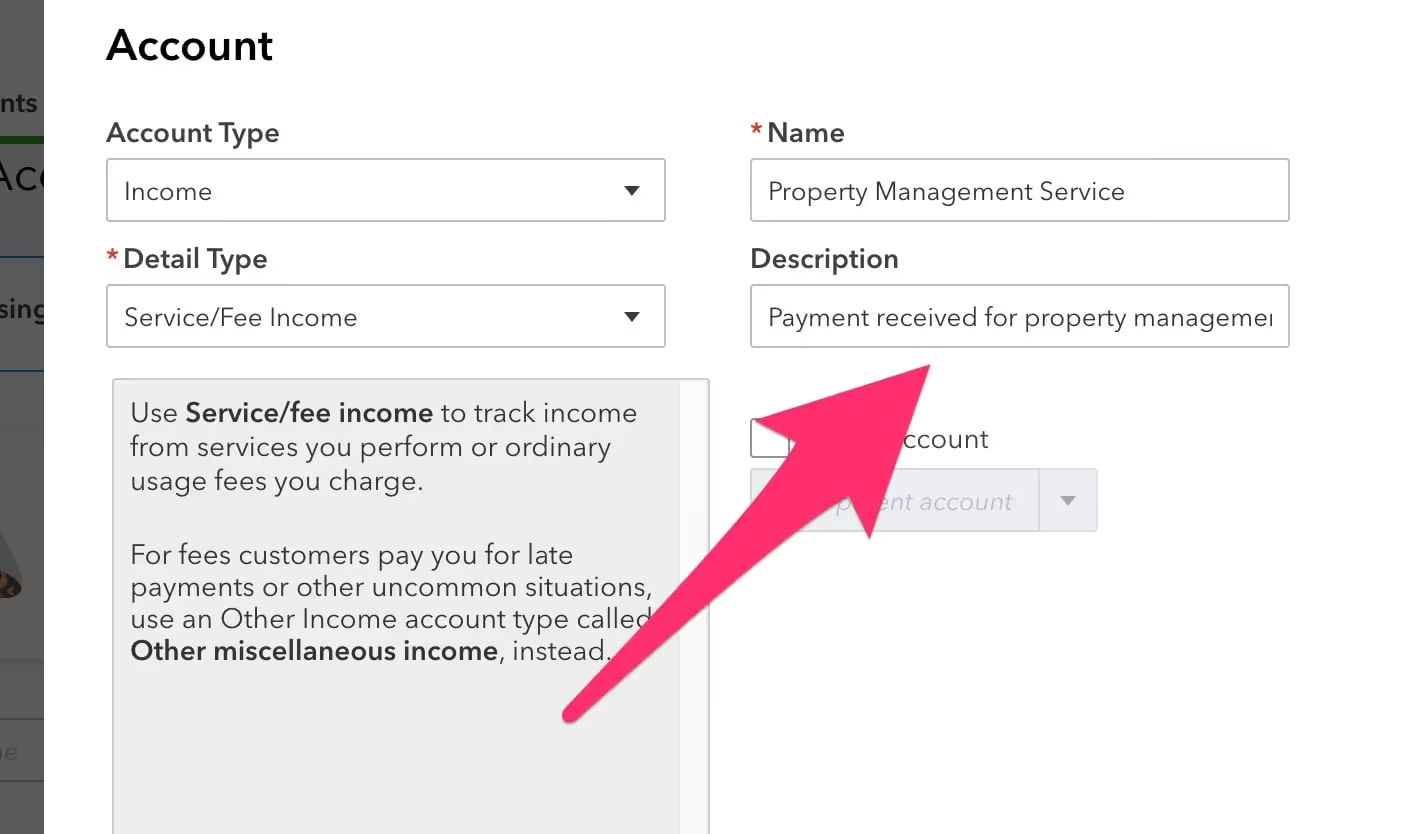

For this example, we’ll create the account you’ll use to receive payments for your property management services.

So, name and describe it in a way that will make it easily identifiable when you run accounting reports.

Like this:

Once you’ve finished creating your accounts, you’ll be able to view them on the chart of accounts page:

Make sure to do this for all relevant accounts, as we touched on earlier.

That could include assets such as equipment, liabilities such as payroll, and expenses such as utilities, rent, and insurance.

3. Add your service(s)

Now, it’s time to make it so you can send invoices.

To do that, you'll first need to create a service. Do that by clicking “Invoicing:”

Click on the “Products and Services” navigation item at the top right:

Then, click “New:”

Once you’re there, fill in the service name (for the sake of the example, we used the easily identifiable “Product Management Services”). Hit save:

4. Create invoices and record income for your property management services

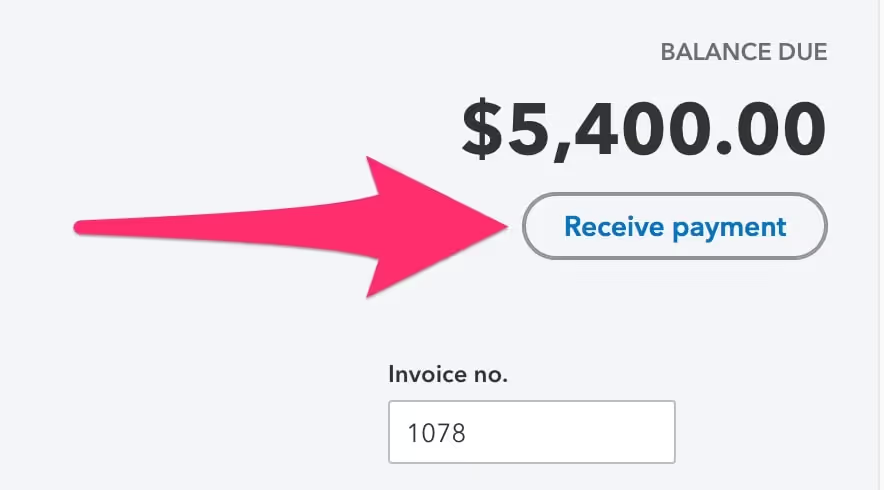

Now you’re ready to generate invoices and accept payments.

Do that by navigating back to the main dashboard and clicking on “Add Invoice:”

Since you’ve already got your client information inputted into QuickBooks by this point, creating an invoice should be pretty quick.

Just click on the customer drop-down, select the client you’re billing, input the amount, any additional notes, and hit send:

Once you’ve received payment, make sure to click on the invoice again and select “Receive payment” so it reflects in QuickBooks:

Now, let’s talk about how to set up your rental property management customer file and associated accounts.

How to Set Up Your Rental Property Management File in QuickBooks

Next, let’s set up the company file you’ll use to manage your properties.

As mentioned earlier, you’ll use this company file to record all transactions related to the properties you manage:

- Collecting rent payments

- Collecting other payments and fees such as pet rent, parking fees, etc.

- Recording security deposits

- Paying for maintenance, repairs, and upgrades

Keep in mind that you’ll need QuickBooks Pro or Premium to have two company files at a time.

So, as a property management company, it’s necessary to properly do property management accounting with a property management software like QuickBooks.

Let’s start with step 1: setting up properties.

1. Set up properties

This is the part where QuickBooks gets a bit difficult.

Because QuickBooks isn’t designed for property management, there's no way to add properties specifically.

Instead, you’ll need to add each property as a customer.

So, once again, click on “Add customer:”

Then fill in the property’s information:

If all you add is the property’s name (this could be the street address or the name if it’s a business park), that’s fine for now.

2. Set up tenants

Now, to add tenants, you’ll need to once again go back to your dashboard, click “Add customer,” and input their information to add each tenant as an individual customer.

I know what you’re thinking: the properties are already customers. What gives?

There’s only a selection for customers in QuickBooks. There aren't properties, tenants, etc.

Again, we will discuss later how other property management software addresses this issue.

But, for now, let’s talk about how to make QuickBooks work.

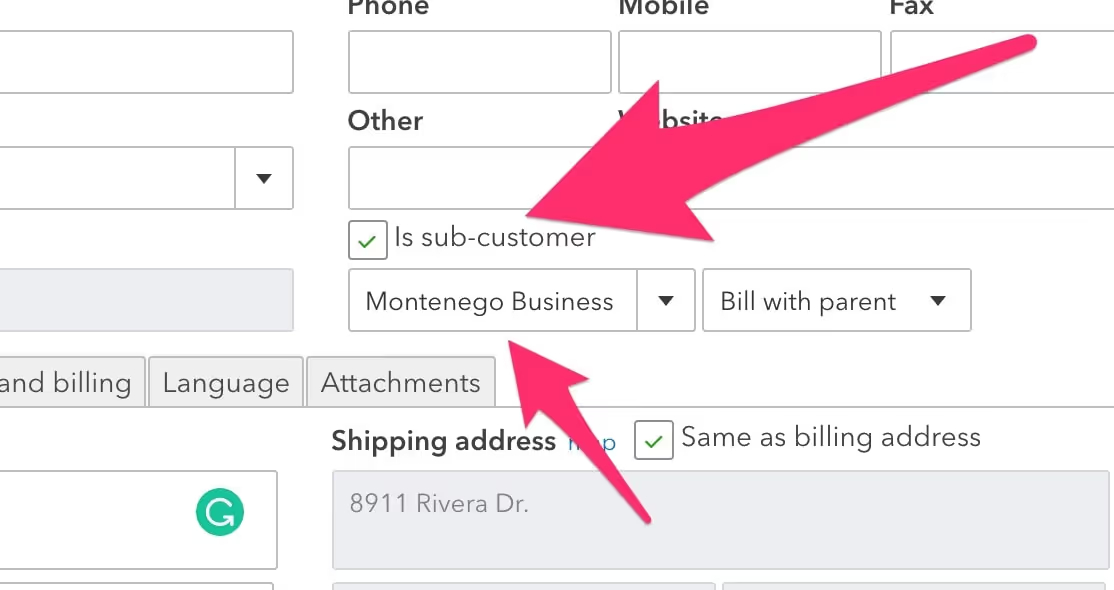

When you click to add each tenant as a customer, you’ll need to make sure to click on the “Is sub-customer” checkbox on the middle-right:

Once you’ve done that, click the drop-down below it and select the property in which the tenant resides.

This will make it so that your customer, Monica Johnson, is shown as a sub-customer under the Montenego property.

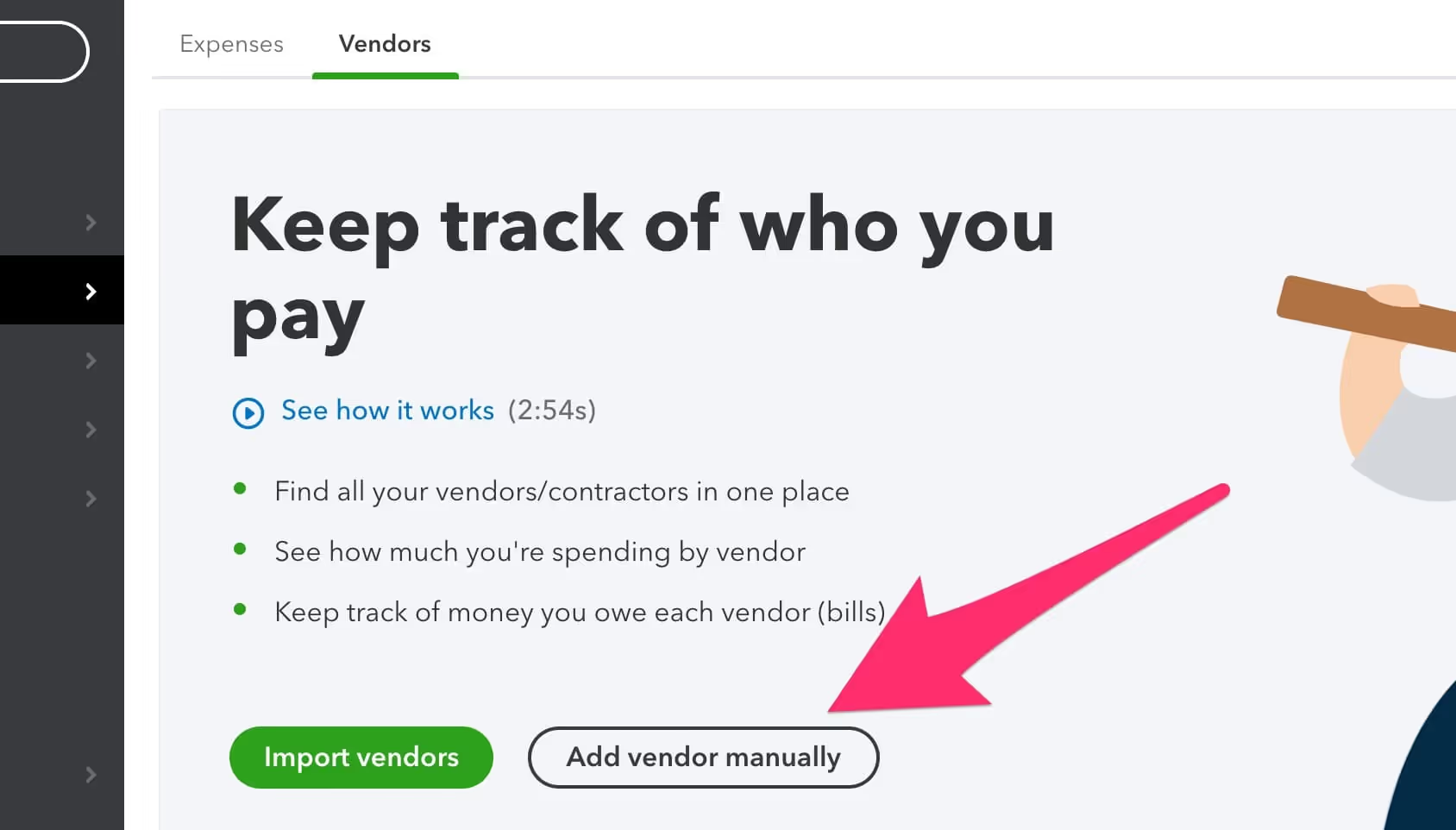

3. Set up owners as vendors

While you’re adding tenants, make sure to add the owners of the properties you manage as well.

This is done in almost the same way but in a different section.

From the main menu, navigate to “Expenses,” then “Vendors.” Then click on “Add vendor manually:”

The process here is nearly the same as adding a customer. So, once you’ve inputted the information you’d like to add, click “Save.”

4. Set up accounts and services

We covered each of these in setting up your administrative-side business activity, so we’ll make this short.

Navigate to “Accounting,” then “Chart of accounts:”

Then, click “New” to create a new account:

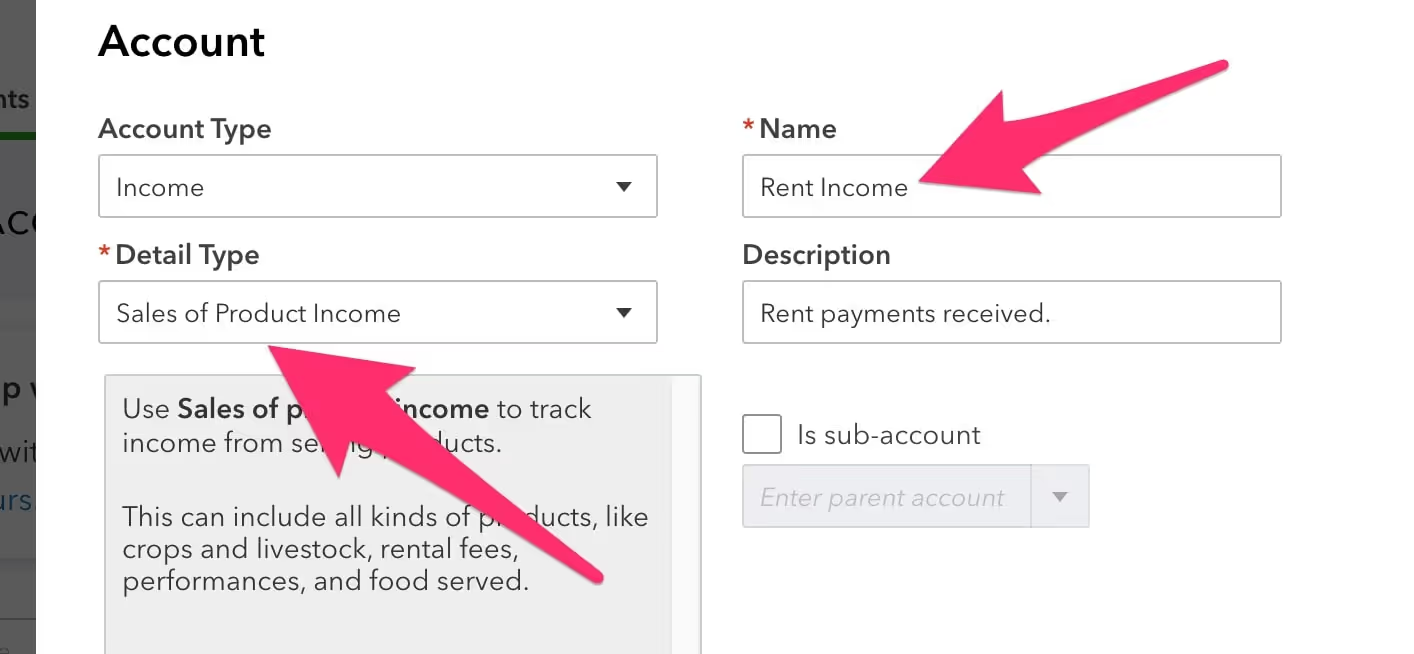

Select the proper primary account from your chart of accounts:

In the last example, we added an account for you to receive payments for your property management services.

In this example, we’ll add an account for rental income that will record all rent payments you receive from tenants:

Again, for here as well, you’re going to want to add an account for all relevant financial activity regarding the managing of your properties.

That includes, but is not limited to, the following:

- Security deposits (under liabilities)

- Pet rent (under income)

- Property owner payment (under expenses)

- Assets, such as bank accounts (under assets)

Once you’ve done this, you can start collecting rent payments by creating invoices, just like we did in the last section.

And, with that, you’re (mostly) set up!

Keep in mind that this isn’t a comprehensive guide to getting started with QuickBooks, but more of a starting point to show you how to get going and help decide if QuickBooks is right for you.

Several additional steps and many more hours are likely necessary to optimize your QuickBooks so that you can use it for everything you’ll need.

With that said, we hope this guide helps you get things off the ground faster and easier, especially if you’re just getting started.

If you’re an established property management company, though, chances are you either want or downright need something with more power and tailored features to fit your property management efforts.

The Limitations of QuickBooks

QuickBooks has a ton of functionality.

There’s a reason why it remains the most well-known business accounting software there is.

However, when it comes to property management accounting, QuickBooks’s limitations show, especially when you compare it to property management-specific software.

Limitation 1: It’s Not Designed For Property Management, So Difficult Workarounds Are Abundant

QuickBooks is great for small and even some medium-sized property management companies.

The larger your company grows, though, the more you’ll find yourself wanting something more specialized.

You might already be in that position.

With QuickBooks, you often have to execute confusing or difficult workarounds like adding both properties and tenants as customers.

This might not seem like a big deal at first, but when you add up the additional time it takes to get everything set up and then realize how difficult it can be to run reports like this, these workarounds start to show their ware.

Limitation 2: Can’t Separate Business Activity Optimally

Property management companies are unique in that they have two facets to their business:

- Financial activity regarding the business itself and administrative tasks, such as paying payroll and expenses such as utilities

- Property management activity having to do with performing the service, such as collecting rent, paying for repairs, and holding security deposits

QuickBooks can’t manage the kind of multi-account system that larger property management companies require to separate payments to owners (which should be kept in its dedicated account separate from all other financials) from expenses, and both of those separated from payments you receive from owners for your services.

This can cause QuickBooks to progressively become a limiting property management software the larger you get.

Limitation 3: Lack of Additional Features (Accounting Only)

As software continues to evolve and develop, new things become possible.

Now, a single piece of software can do everything from managing your accounting to the following and more:

- Remind you when leases are about to expire so you can maintain occupancy

- Manage work orders and schedule maintenance calls

- Maintain multiple bank accounts with separate finances, from expenses to security deposits, owner payouts, and your own company payments

QuickBooks does what it does well. It’s arguably the most comprehensive accounting solution out there.

But property management software includes a whole suite of features that QuickBooks just can’t match on its own.

Not to mention, property management software is built specifically for property management accounting.

Strictly for accounting, QuickBooks can serve as a perfect solution if you run or are a part of a small- to medium-sized property management company.

However, if you’re larger, consider what property management software can do for you and what features would be most helpful.

What Unique Features Can You Find in Property Management Software?

If you’ve realized that QuickBooks could be limiting you—whether it’s because you manage hundreds or thousands of properties and you want a custom solution that will save you time and headache, or you find the added features useful—then you have good reason to look into property management software to replace QuickBooks.

Consider these points when looking at the various features that property management software offers and which matter most to you:

- What improvements you feel you can make to your operation

- What your biggest time-wasters are

- Which features will offer the highest return on your investment

Property management software like DoorLoop typically has several invaluable features that go far beyond basic accounting. Here are some examples:

- A tenant portal where tenants can pay their rent, select rental insurance, and even make and communicate with you on maintenance requests

- An owner portal where owners can review the performance of their property

- Built-in tenant screening, so you can screen and set up new tenants all from the same tool

- Tools for scheduling property showings and listing your property online

And that’s just scratching the surface.

But the point is this: by figuring out which features are most helpful to you and your team, you’ll be able to figure out which kind of software is best for your business.

What Will You Use to Power Your Property Management Business?

Only you can decide what the best solution is for you between these options:

- QuickBooks

- A dedicated property management software solution like DoorLoop

- Both together, if you want the valuable features of property management software but need specific accounting features from QuickBooks

One thing is for sure: you need a great accounting tool that will help you not only manage your business but also maximize its performance.

Property management software isn’t a dedicated accounting solution, though it can replace QuickBooks entirely in many cases.

In fact, with DoorLoop, you can do it all, including these tasks and more:

- Create financial statements

- Design custom reports

- Print checks

- Collect rent by credit cards, ACH, and more

So... whether you need robust accounting features built with property managers and landlords in mind, or you’re looking for a full suite of tools to optimize your entire operation, let DoorLoop help streamline your operation by bringing everything together into one easy-to-use platform.

Schedule a free demo today to experience DoorLoop for yourself!

Whatever you choose, we hope this guide helped you clarify how QuickBooks works for property management accounting and discover your options for property management software.

Frequently Asked Questions

What features does property management software have that QuickBooks doesn’t?

Property management software includes features that QuickBooks doesn’t offer, such as tenant portals, lease tracking, maintenance request management, and automated rent reminders. These tools are built specifically for day-to-day property operations, helping landlords and managers streamline tasks beyond basic accounting. QuickBooks focuses mainly on financial tracking and lacks the operational tools needed to manage tenants and properties efficiently.

Can property management software handle accounting as well as QuickBooks?

Many property management software platforms include built-in accounting tools that cover essential functions like rent tracking, expense management, owner statements, and bank reconciliation. While QuickBooks may offer more advanced general accounting features, property management software is often sufficient for landlords and tailored to their specific needs.

Do I need both QuickBooks and property management software?

You may not need both QuickBooks and property management software, especially if your property management platform includes built-in accounting features. However, some landlords prefer to use both, combining the operational tools of property management software with the advanced financial reporting of QuickBooks. Platforms like DoorLoop offer seamless integration with QuickBooks to support this setup.

Which is more cost-effective, QuickBooks or property management software?

QuickBooks is generally more affordable upfront, especially for basic accounting needs, but it may lack key features required for managing properties. Property management software often includes tools like rent collection, maintenance tracking, and tenant communication, which can save time and reduce the need for additional services. For landlords or managers with multiple units, the all-in-one functionality of property management software may be more cost-effective in the long run.

How does each option scale as my portfolio grows?

As your portfolio grows, QuickBooks can become harder to manage due to its limited property-specific tools and manual setup for tracking multiple units. Property management software is designed to scale more efficiently, offering features like bulk tenant communication, automated rent reminders, and multi-property reporting. This makes it easier to stay organized and reduce administrative workload as your business expands.