Trust accounts are a valuable tool that make compliance as a property manager easier. However, when it comes to property management trust accounting, the details can get complicated quickly.

There are tons of potential compliance issues, legal pitfalls, and varying state laws to watch out for—and all of these things could land you in hot water. Still, when properly set up, your tenant’s funds are safe, and you’re protected against judgments and audits.

In this updated guide for 2026, we’ll detail exactly how trust accounts work, the strict rules regarding deposit timing and record retention, and how to keep your books audit-ready.

Key Takeaways

- Separation is mandatory: Never mix (commingle) your business operating funds with client funds (rent, deposits, reserves).

- Timelines are tight: While laws vary, many states (like North Carolina and Oregon) require deposits within three banking days.

- Three-way reconciliation is vital: You must match your bank balance, checkbook balance, and the sum of all client ledgers every single month.

- Records are forever (almost): Depending on your state (e.g., Texas, Florida), you may need to retain records for 4 to 6 years.

- Software simplifies compliance: Tools like DoorLoop automate reconciliation and ensure separate ledgers are maintained automatically.

What Is Property Management Trust Accounting?

In plain English, property management trust accounting is the practice of holding and managing funds on behalf of a third party (your property owners and tenants) in a specifically designated bank account, completely separate from your own business capital.

The purpose is straightforward: In property management, a trust account is used to keep tenant rent payments, security deposits, and maintenance reserves safe and separate from your company's operating funds, with balances reflected across a tenant management suite.

This ensures that if your property management company were ever to face legal action or bankruptcy, the money belonging to your clients and tenants remains protected.

What money belongs in a trust account?

Generally, any money that does not belong to you should go here, tracked cleanly in a property management accounting software like DoorLoop. Common examples include:

- Rent payments collected from tenants.

- Security deposits (often required to be in a separate account).

- Maintenance reserves funded by owners for repairs managed through work order software.

- Advance rent payments.

Why Trust Accounting Matters for Property Managers

Trust accounts are required by law in almost every state. Beyond the legal requirement, you want a trust account to keep your accounting domains organized.

Property managers need to simultaneously manage two separate accounting spaces:

- Your business accounting (Operating Account)

- Each property’s accounting (Trust Account)

Mixing things like your monthly office rent, payroll, and client payments in with the same account you use to collect rent payments is a big no-no. That’s mainly because the beneficiaries are different.

- When it comes to your business activity, you’re the beneficiary.

- When it comes to the properties you manage, the owner is the beneficiary.

Regulators explicitly flag trust fund handling violations as a top enforcement priority. For example, recent advisories from the California Department of Real Estate (DRE) and the North Carolina Real Estate Commission (NCREC) highlight that failure to maintain separate records is a primary reason for audits and license suspensions.

Trust Accounting Rules Property Managers Must Follow

While using a trust account comes with benefits, there are potential pitfalls to watch for regarding compliance.

1. Strict Deposit Timelines

The most common mistake is holding onto checks too long. While some older guides suggest a generic "24-48 hour" rule, the reality depends on your specific state statutes.

- Common Rule: Many states, such as North Carolina and Oregon, generally require trust funds to be deposited within three banking days of receipt.

- Best Practice: Don't wait. Deposit funds daily to avoid "constructive commingling" accusations.

2. Commingling of Funds

Easily one of the trickiest aspects is avoiding commingling. This refers to any situation where owner funds mix with property manager funds.

Examples of commingling include:

- Depositing trust funds into a personal or business operating account.

- Depositing personal or business funds into the trust account (except for a small amount to cover bank service fees, if allowed by your state).

- Leaving your earned management fees in the trust account for an extended period (check your local laws on the exact timeline to withdraw your fees).

- Using one client's funds to pay for another client's repairs (negative ledger balances).

3. State Laws on Account Quantity

Some states allow—or require—multiple trust accounts. For example, you might need:

- An “operating” trust account for rent and expenses.

- A separate trust account strictly for security deposits.

Recordkeeping and Separate Ledgers

To protect yourself from audits, you must keep records of everything. A good bookkeeping software can help. It is not enough to just have a bank statement; you need a separate sub-ledger for every property and owner, which is a core requirement in rental property accounting software.

State regulators like the Texas Real Estate Commission (TREC) and the Florida Real Estate Commission enforce strict retention periods. You generally need to keep records for 4 to 6 years, depending on where you operate.

Note: Always consult your specific state real estate commission for the most current rules.

How to Set Up a Property Management Trust Account

Setting this up correctly with your bank is the first step toward compliance.

Dos

- Do title the account correctly: The words "Trust," "Escrow," or "Client Benefit" should appear in the official bank account name. This is often required for FDIC pass-through insurance coverage, which protects each individual owner’s funds up to the limit, rather than just the account total.

- Do separate security deposits: If your state requires it, open a completely distinct account for deposits versus rent.

Don'ts

- Don't rely on "nicknames": Just renaming an account "Trust" in your online banking dashboard isn't enough. The legal titling on the bank's signature card must reflect its status.

- Don't add unauthorized signers: Limit access strictly to licensed brokers or authorized personnel.

Trust Accounting Best Practices

Accounting is rarely fun, but it’s a necessary part of any sound business venture, and choosing a real estate accounting software can make it more manageable. Follow these best practices to stay audit-ready:

- Reconcile Monthly: Even if your state doesn't explicitly mandate it, performing a reconciliation every month is the only way to catch errors before they compound, especially with bank sync.

- Implement Internal Controls: Require dual approval for large disbursements and separate the duties of who collects rent and who writes checks.

- Backup Documentation: Keep digital copies of every lease, deposit slip, vendor invoice, and owner report.

Common Trust Account Transactions

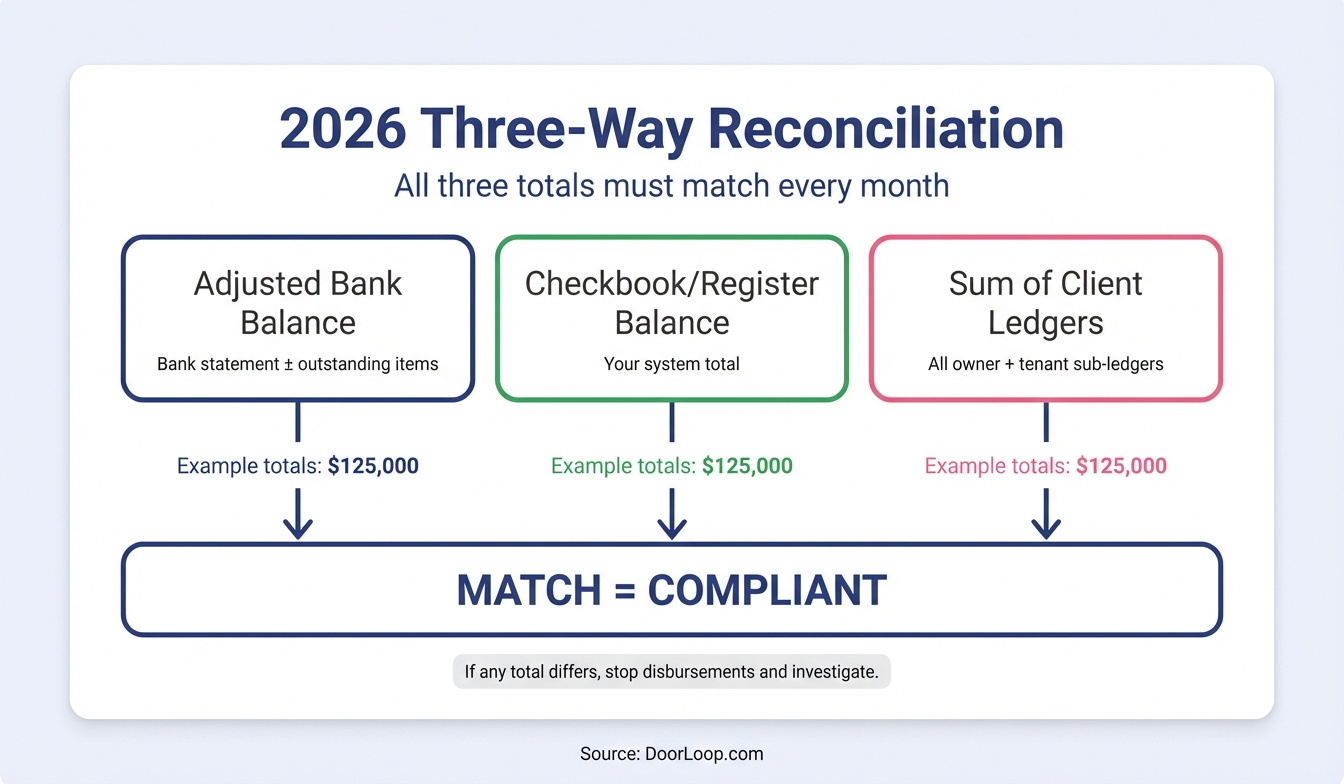

Three-Way Reconciliation and Trust Account Audits

If you only take one thing from this guide, let it be Three-Way Reconciliation. In standard accounting, you match your bank statement to your checkbook, with a consistent chart of accounts supporting accurate categorization. In trust accounting, you must match three numbers:

- The Adjusted Bank Balance: What the bank says you have (plus/minus outstanding checks/deposits).

- The Checkbook/Register Balance: What your system says the account total is.

- The Sum of Client Ledgers: The total of all individual balances for every owner and tenant you manage.

If these three numbers do not match exactly, you are out of compliance. Regulators, including the California DRE, cite failure to reconcile regularly as a primary violation.

How Property Management Software Makes Trust Accounting Easier

If you’re working with traditional checks or spreadsheets, maintaining a three-way reconciliation is a massive headache. Fortunately, a better way exists.

With a tool like DoorLoop, you can collect rent automatically and have it immediately deposited into the correct account. DoorLoop is built with trust accounting compliance in mind:

- Automated Bank Sync: Transactions are categorized instantly.

- Audit-Ready Reports: Generate owner statements, balance sheets, and rent rolls in one click.

- Safety Controls: Set permissions so unauthorized staff cannot move funds.

- QuickBooks Integration: Sync data effortlessly with QuickBooks Integration to keep your accountant happy.

Pricing is straightforward, with plans starting at $69/month (billed annually) for your first 20 units. No manual work, no hassle.

See how DoorLoop helps you manage all your property accounting from one place.

Get your accounts in order

By getting your accounts in order and making sure you’re using properly titled trust accounts, you’ll save yourself a ton of potential headaches and legal exposure. Remember to check with your state and local laws to be clear on what exactly you need to do to be compliant.

Ready to simplify your accounting? Request a demo today to see how easy it can be.

Sources

- FDIC – Pass-through Deposit Insurance Coverage

- North Carolina Real Estate Commission – May 2025 Bulletin

- Oregon Real Estate Agency – Security Deposits: A Compliance Reminder

- Texas Real Estate Commission – Record Retention Rules

- California Department of Real Estate – Most Common Enforcement Violations Advisory (2025)