Key Takeaways

- For multifamily operators, amortization shows how each mortgage payment splits between principal and interest, which affects cash flow, equity, and refinancing timing.

- A $200,000 loan at 5% costs about $186,512 in interest over 30 years, compared with about $84,686 over 15 years.

- A 30-year term lowers the monthly payment to about $1,073.64, while a 15-year term raises it to about $1,581.59 and builds equity faster.

- Accelerated amortization can reduce total interest without committing to a shorter loan, but confirm extra payments apply to principal and avoid prepayment fees.

Understanding how your monthly mortgage payments work and what they go towards is a little trickier than people first think.

Paying a mortgage is more complex than splitting the total loan amount into monthly chunks- there is also the interest rate to think about.

This guide to mortgage amortization provides a simple overview of how to calculate your mortgage payments and how much goes toward interest over the actual loan- including examples and a few other useful things to know.

What Is Mortgage Amortization?

In a nutshell, mortgage amortization is the gradual repayment process on a loan, where each payment goes partly toward the amount borrowed and partly toward interest.

As the payments continue, the amount allocated to each part changes- with higher interest payments at the beginning- and higher principal payments (the actual amount borrowed) as your loan matures.

An amortized loan usually has a fixed rate and is paid back over a 15 to 30-year time frame. Calculating your loan amortization helps you see how much interest you will pay over the life of the loan.

It is important to understand how amortization calculations work- so you know how much interest you have paid and how much is left on the balance- especially if you are considering re-mortgaging or making any extra payments.

How Are Monthly Mortgage Payments and Mortgage Amortization Calculated?

The calculation for loan amortization is quite complex and differs depending on whether you have a fixed-rate mortgage or adjustable-rate mortgage.

Either way, there are three main components used to calculate amortization on a mortgage loan.

- The amount borrowed

- The loan term

- Your annual interest rate

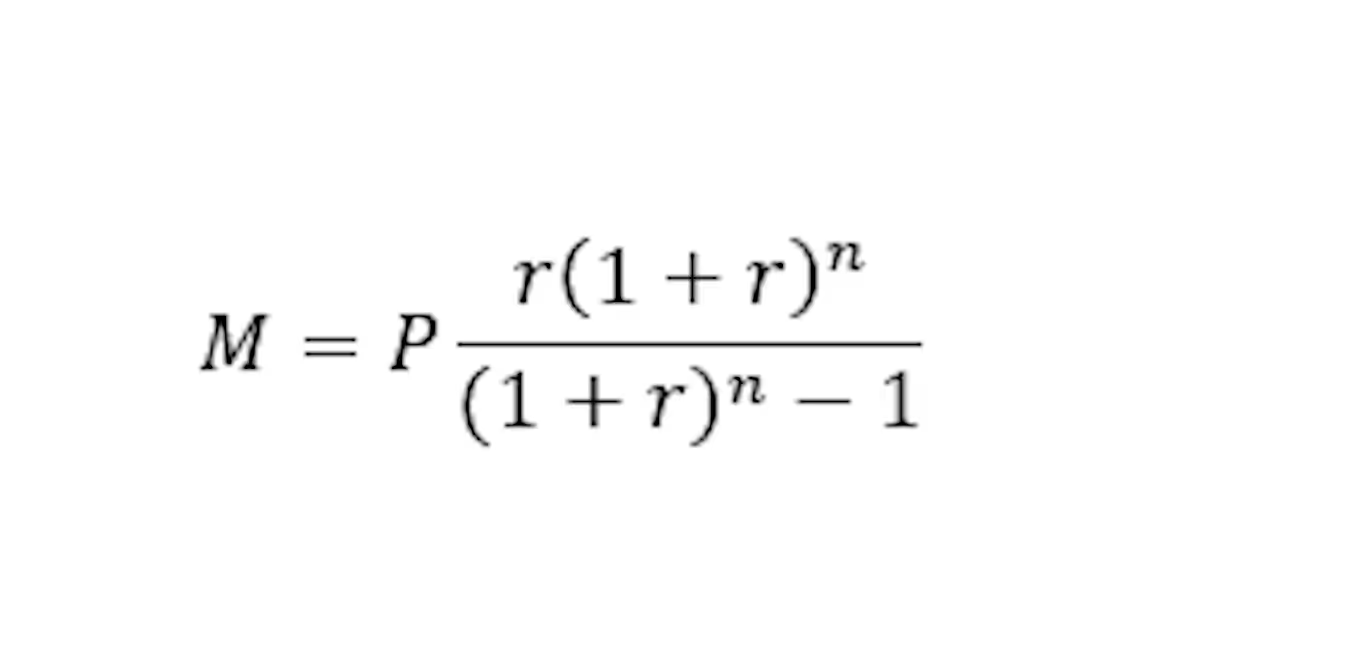

Your monthly payments are worked out based on the total amount you need to repay, plus the annual interest rate split into 12 months, divided by the total number of months in your loan term.

The variables you need for the calculation are:

- P: Principal loan amount

- r: Monthly interest rate (most loan companies provide an annual rate, so you need to divide it by 12 first)

- n: Total number of payments (multiply the number of years in your loan by 12 months- assuming you make monthly payments)

It looks like this:

From there, an amortization schedule calculator works out the estimated monthly split between principal and interest for the duration of your loan.

What Is a Loan Amortization Schedule?

Your amortization schedule is the projected monthly amount that will go to principal and interest for the duration of your loan. It tracks how much interest you will pay each month and how much equity you will pay back into your property.

As you move through the amortization table, you can see cumulatively how much interest is paid and how much of the loan balance you still need to pay.

What Impacts Monthly Payments and Mortgage Amortization?

Amortization is most affected by loan terms. The more monthly loan repayments you need to make- the more interest you will pay.

It is also impacted by the type of mortgage you have. Fixed-rate mortgages maintain the same interest rate until the loan matures, but adjustable-rate mortgages may change after some time.

Other factors that may influence your mortgage payments and amortization schedule include:

- The down payment amount

- Lump sum payments

- Additional payments toward the principal balance

- Mortgage insurance

- Property taxes

- Homeowners insurance or landlord insurance

- Other costs and fees

Applying Amortization to the Rental Property and Real Estate Market

Let's look at an example of loan amortization in the world of property investment.

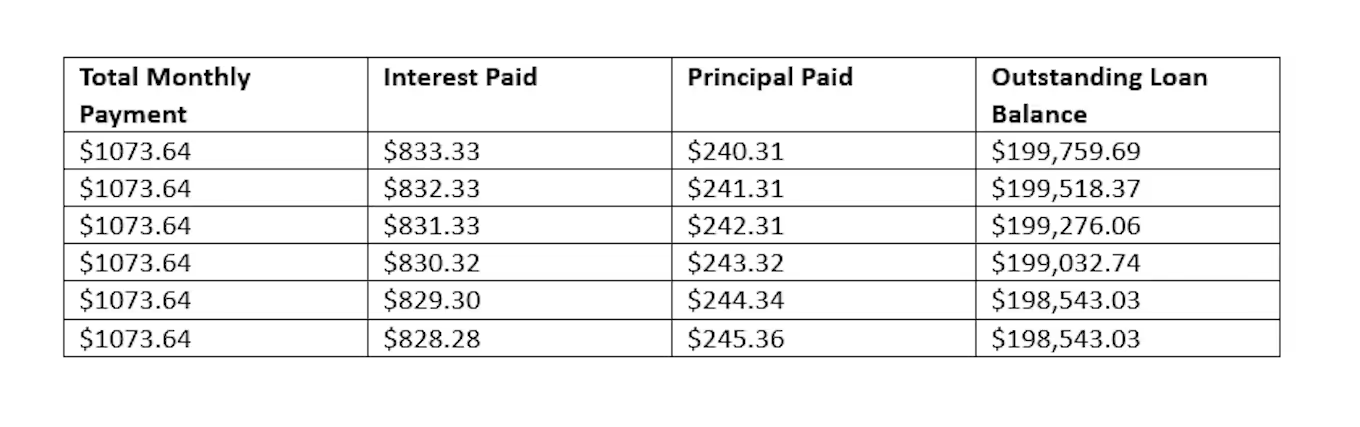

If you borrow $200,000 at 5% interest in a 30-year loan, your estimated monthly payment would be $1,073.64, and the total interest owed would be $186,511.57.

The first six months of your amortization schedule may look like this:

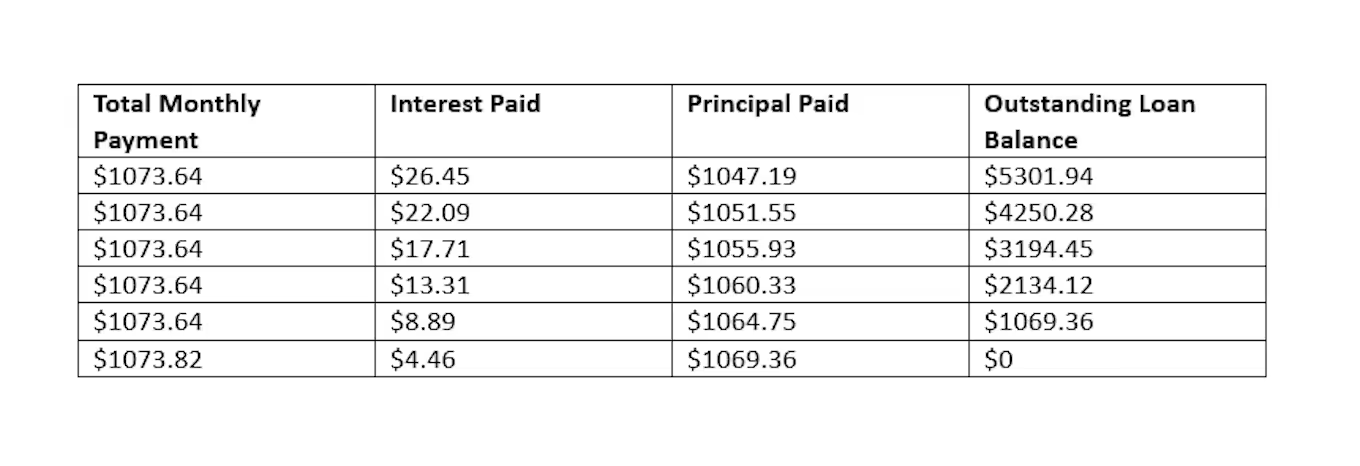

By the final six months, the payments would look more like this:

Take the same loan amount and interest rate but change the loan term to 15 years instead of 30, and the total amount of interest paid drops significantly to just $84,685.71. However, the monthly payment is much higher- at $1581.59.

The schedule would be similar- but with a more even split between principal and interest payments from the beginning.

Using real estate calculators is the easiest way for property managers and investors to figure out what their monthly expenses are and much more.

Leveraging Mortgage Amortization: Strategies to Consider

Choosing the best amortization schedule and strategy comes down to how much you can afford to pay each month and how quickly you want to own your home.

Short Term VS Longer Term

There is no question that a shorter loan term is favorable in terms of the total interest you will pay, but the higher monthly mortgage payments are not manageable for everyone.

Choosing a 15-year term over a 30-year loan means paying significantly less in interest and build equity in your property much faster. A $200,000 loan with a fixed interest rate of 5% would cost roughly $186,500 in interest over 30 years but less than $85,000 over 15 years.

However, the monthly payment on a 15-year loan would be close to $1,600- an amount that could be unfeasible for most.

When choosing the term of your loan, consider the financial strain a higher monthly payment would put you under. It is not always worth pushing it to the limit every month- especially when there are ways to shorten your loan term if you have some spare cash.

Fixed Rate VS Adjustable Rate Mortgages

The next thing to consider regarding your mortgage strategy is whether you want a fixed or adjustable interest rate. Most people opt for fixed rates on their amortized loans.

Having an adjustable rate could provide more flexibility with payments later in the mortgage, but it could also leave you with a sudden hike in price that you can't keep up with.

If you can get a decent interest rate, it is generally advisable to go for a fixed mortgage for stability and predictability. Of course, you should speak with an advisor and make the choice you feel is right for you.

Accelerated Amortization

You also have the option to pick a longer loan term (to benefit from lower monthly payments) but use accelerated amortization to pay off the principal balance sooner.

This works by allocating additional payments to your standard mortgage payment that go solely toward the principal.

Some people make biweekly payments instead of monthly, pay a little extra every second month, or make an annual lump payment toward the outstanding principal amount.

The most important things to remember with accelerated payments are:

- Make sure your lender processes the additional payment correctly so it only goes towards the principal payment.

- Check with your lender how much extra you can pay without incurring any charges.

- Consider whether it is worth using the extra cash to go towards the mortgage payment or whether it would be better used as an emergency fund.

What Does a Good Amortization Schedule Look Like?

The best amortization schedule for one person is not necessarily the best for another. It depends on their priorities and financial situation.

What matters the most is having the correct balance between an affordable monthly payment and keeping the total interest as low as possible.

If you don't want to pay a huge amount of interest but are limited to what you can afford each month, the best idea is to take out a smaller mortgage loan, to begin with- or pay as much as you can as a down payment before the schedule is worked out.

Other Things to Know about Amortization and Your Mortgage Payment

- It is possible to recast your mortgage later in the term, which essentially recalculates the amortization schedule. This is a cost-effective alternative to refinancing, which starts a whole new amortization schedule that reverts to paying high amounts of interest.

- Your loan's amortization period does not affect the actual interest rate- only how much the total of your interest will be. A fixed annual rate of 5% stays at 5% whether you pay it back over five or 50 years, but how much interest it accumulates varies, based on how quickly the principal is paid.

- Figuring out the schedules for fully amortizing loans is complicated, but with a mortgage calculator, you get an estimate in seconds.

How Can DoorLoop Help?

As a property investor, there are many more things to handle on top of your mortgage payments and amortization schedule. If you own rental properties or plan to invest in the real estate market as a landlord or property manager, you need a tool that helps you across the board.

DoorLoop is that tool- providing a comprehensive space to manage your property portfolio no matter how big or small.

Using the advanced suite of accounting tools, you can keep track of income and outgoing- including the money you are making from rent and how much is going towards paying off your mortgage.

Track if and when you can make extra payments based on your financials, and stay on top of timely payments with automated reminders and schedule planning.

DoorLoop also provides a range of real estate calculators that help property owners working in the rental market keep on top of their finances.

Some of the Other Great Features Available Through DoorLoop

- Tenant screening and application management

- Marketing

- Automated online rent collections

- Maintenance management

- Lease management

- Tenant portal

The list goes on. DoorLoop has a lot to offer- see for yourself by scheduling a free demo and explore the possibilities.

Summary

A loan amortization calculator is the fastest and easiest way to establish your repayment schedule and total interest. Remember to compare interest rates from different lenders and think about how much you can afford each month without putting your business and personal finances under strain.

Frequently Asked Questions