Key Takeaways

- For multifamily operators, the IRS taxes rental income as ordinary income, including rent, advance rent, retained deposits, tenant-paid expenses, and lease cancellation payments.

- Track deductible operating costs carefully, because property tax, insurance, advertising, mortgage interest, repairs, maintenance, utilities, and qualifying supplies can materially reduce taxable income.

- Depreciation can produce major savings: residential buildings depreciate over 27.5 years, while commercial buildings use 39 years, excluding land value.

- In the 15-unit example, deductions and depreciation lowered taxable rental income from $216,000 to $134,546, cutting estimated tax from $47,520 to $29,600.

Buying and managing rental properties is a tried-and-true investment.

But with every great investment opportunity comes Uncle Sam, waiting to collect.

That’s why understanding rental income tax is so important.

The better you understand how rental income tax works, the better prepared you’ll be when tax time comes.

Not to mention, the more you can structure your taxes in a way that you minimize that tax burden.

In other words, you pay less taxes... and keep more money in your pocket.

Tax time might feel like something to dread.

But with all the deductions and even special tools you can (legally) take advantage of, you’ll be looking forward to tax time rather than avoiding it.

Let’s not get ahead of ourselves, though.

First, let’s start from the top: How does rental income tax work?

Then, we’ll talk about reductions you can take advantage of, and finally end with an example so it’s crystal clear how rental income tax is calculated.

How is rental income taxed?

First, let’s talk about how rental income tax works.

The short and sweet answer is:

Rental income is taxed like ordinary income you’d generate from any 9-5 or personal business.

So, for example: if you’re in a 25% tax bracket and generate $50,000 in rental income, you’d pay $12,500. You can also use online calculators to determine this amount.

Pretty easy, right?

Easy to understand, but you might not like having to pay $12,500, though.

Fortunately, it’s at this point that the difference between ordinary income and rental income diverges.

In terms of potential deductions, rental income is much more like business income.

That’s because there are dozens of various deductions and other methods for lowering your tax burden.

What is considered rental income?

Now that we’ve covered how rental income is taxed (basically), let’s dive in deeper to talk about how to calculate your rental income based on IRS standards.

According to the IRS, rental income is “any payment you receive for the use or occupation of property.”

The important part of this is that it doesn’t just include monthly rent you receive from tenants.

Rental income comes in several forms, including:

1. Monthly rent payments

Monthly rent received from tenants, the most atypical.

2. Advance rent payments

Even if you receive advance rent payments for next year, the income counts for this year.

3. Security deposit money retained

Any portion of the security deposit that you do not give back to the tenant counts as rental income, as security deposits count as advance rent.

4. Tenant services

If you rent out a single-family residence to a family who then pays for their own maintenance and deducts the cost from their rent, that amount they covered still counts as rental income tax for you.

This counts for bills and expenses such as the electric or water bill as well.

5. Cancelled lease payments

If your tenant pays you to cancel a lease prematurely, the full amount of said payment is considered taxable rental income.

How to reduce your rental income tax

At this point, you’re probably thinking what we’re thinking:

“I understand how rental income tax works now. So... what can I do to reduce how much rental income tax I pay?”

Good question.

Before you meet with Uncle Sam, there are a few things you can do (both pre-emptively and retroactively.

Let’s talk about them now.

1. Utilize rental income tax deductions

While taxes are never an exciting topic, there are an assortment of tax deductions you can take advantage of to reduce your tax burden.

Here’s a list of some of the most common things you can deduct to lower your rental income tax burden:

- Property tax

- Insurance costs

- Repairs and maintenance

- Other operating expenses

In terms of operating expenses, that includes interest, advertising, maintenance and repairs, utilities, insurance, and even the cost of some supplies purchased with the express purpose of maintaining your property’s condition.

However, on that note, you generally can’t deduct the cost of property improvements, as those are not considered maintenance expenses.

Learn more about what can be deducted in terms of property updates at the official IRS page here: Tangible Property Final Regulations | Internal Revenue Service.

2. Deduct depreciation

Another big deduction we left for its own point is depreciation.

That’s because it’s one of the best rental income tax reduction opportunities, and needs its own section offering a bit of explanation.

Depreciation alone can allow you to go from owing tax to showing no rental income at all on your taxes, and reducing your tax burden to zero.

Depreciation comes in with larger purchases that have a long life.

For example, the purchase of a maintenance vehicle that costs $10,000 and has a useful life of five years can save you $2,000 in depreciation deductions.

That’s because you can deduct up to 20% of the total value of the equipment (minus the salvage value).

Similarly, both residential and commercial properties depreciate, and that depreciation can be deducted on your taxes.

Residential and commercial properties are deducted using a different lifespan, as listed below:

- Residential: 27.5-year life span

- Commercial: 39-year life span

For residential property, you take the cost of acquiring the property, subtract the value of the land, and divide it by 27.5 to figure out how much you can claim in deductions for that tax year.

Depending on the value of the property, that can easily add up to several thousand– or even tens of thousands– of dollars in deductions.

For example, let’s say you own a property worth $500,000 and the value of the land is $75,000.

You’d take the remaining $425,000 and divide that by 27.5%, which equals a $15,454 total depreciation deduction.

If your rental income for the year was $170,000 after deducting expenses, and you’re at a 25% bracket, you’d pay $42,500 before deducting depreciation.

After deducting that $15,454 from your taxable rental income, however, your taxable rental income would be just $154,546.

So, you’d owe just $38,636 as opposed to $42,500, saving you nearly $4,000 in taxes.

Read this page for a more detailed explanation on how rental depreciation deductions work from the official IRS website: Publication 946 (2020), How To Depreciate Property | Internal Revenue Service.

3. Qualified Business Income deduction

Thought that was it? Fortunately, no!

There is yet another valuable deduction you can take advantage of, referred to as the Qualified Business Income tax deduction.

The Qualified Business Income (or QBI) allows you to deduct up to 20% of your pass-through business income.

What is pass-through income?

That refers to any income generated from a pass-through entity, like a Corporation. Lucky for us, investment property counts here.

Just keep in mind that:

- There are limits: $163,000 income threshold for individual taxpayers and $326,600 for married taxpayers.

- It’s complicated: Even if you’re beyond the threshold, you can still claim a partial deduction in some cases.

Read here for the full breakdown on how the Qualified Business Income deduction works via the official IRS page: Qualified Business Income Deduction | Internal Revenue Service.

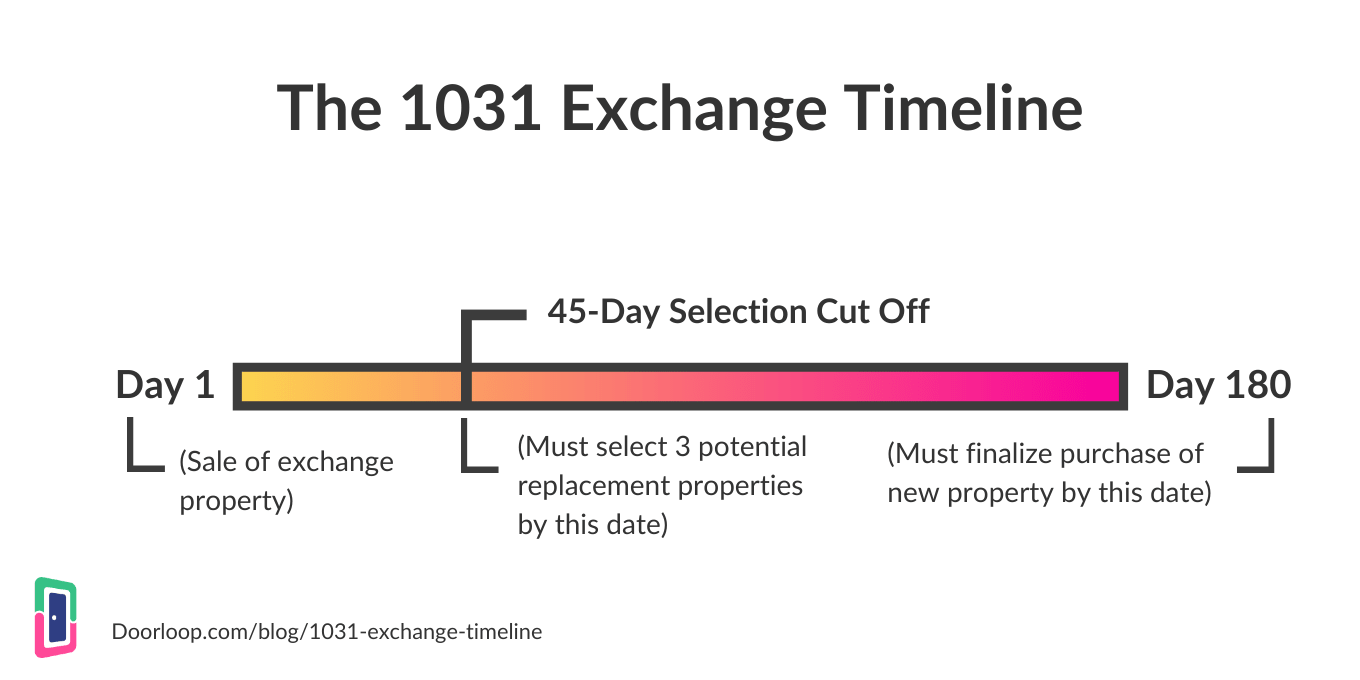

4. Use 1031 exchanges to avoid taxation

In addition to tax deductions and depreciation, there’s another (in this case, pre-emptive) step you can employ to help you reduce your tax bill: a 1031 exchange.

A 1031 exchange is a method of exchanging “like-kind” property, allowing you to defer capital gains tax indefinitely.

By using a 1031 exchange when selling a property, you’re able to avoid having to pay capital gains as well as depreciation recapture taxes.

This point is only relevant when selling a property, but it’s worth considering, particularly if you plan to purchase a different property using the funds of that sale or within the same time frame.

To learn more about how 1031 exchanges work and how they can allow you to defer part of your tax burden, check out our ultimate guide on 1031 exchanges: IRS 1031 Exchange Rules for 2021: Everything You Need to Know.

How to calculate rental income: example

Now that we’ve covered:

- What rental income is

- How it’s taxed

- And ways to reduce how much rental income tax you owe

… let’s go over an example.

Let’s keep this simple and say you have one residential property. An apartment complex with 15 units, we’ll say.

We’ll assume that your property breaks down as follows:

- Type: Residential

- Property value: $475,000

- Lot value: $50,000

- Units: 15

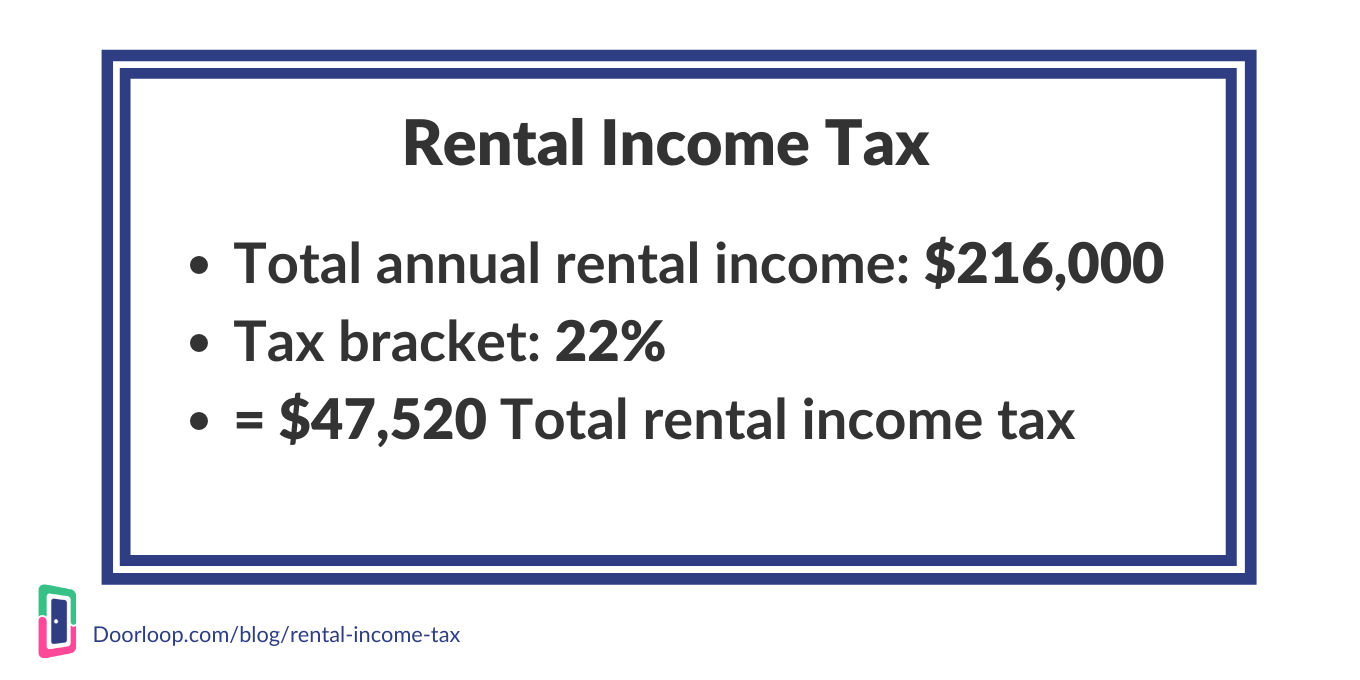

- Total annual rental income: $216,000

If you’re in a 22% tax bracket, you’d be paying $47,520 in rental income tax for the year on that property.

That’s without any deductions. So, let’s add those now.

Rental income tax example: Deductions

Let’s also say that you have a variety of expenses from maintenance to marketing:

- Property tax: $4,750 (roughly 1% annually, depending on where you live)

- Insurance: $12,000

- Advertising: $6,000

- Mortgage interest: $24,000

- Repairs and maintenance: $15,000

- Equipment purchase: $12,000

Now, you can’t write off 100% of the value of every expense.

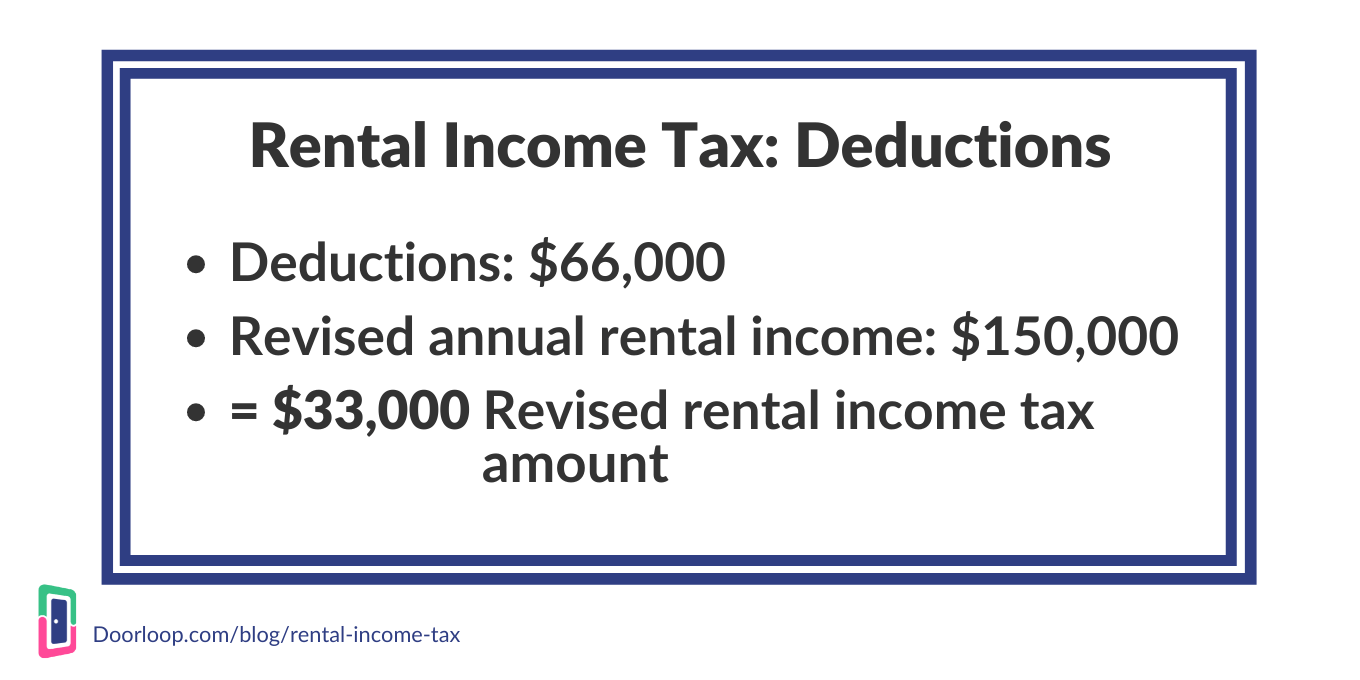

However, for the sake of simplicity, let’s assume that you’re able to write off $66,000 of valid business expenses designed to maintain the property.

You’re now at $150,000 taxable rental income.

At this point, at a 22% bracket, you’d now be paying just $33,000.

In other words, you’ve saved nearly $15,000 in taxes from deductions.

Now, let’s add in depreciation and see where we end up.

Rental income tax example: Depreciation

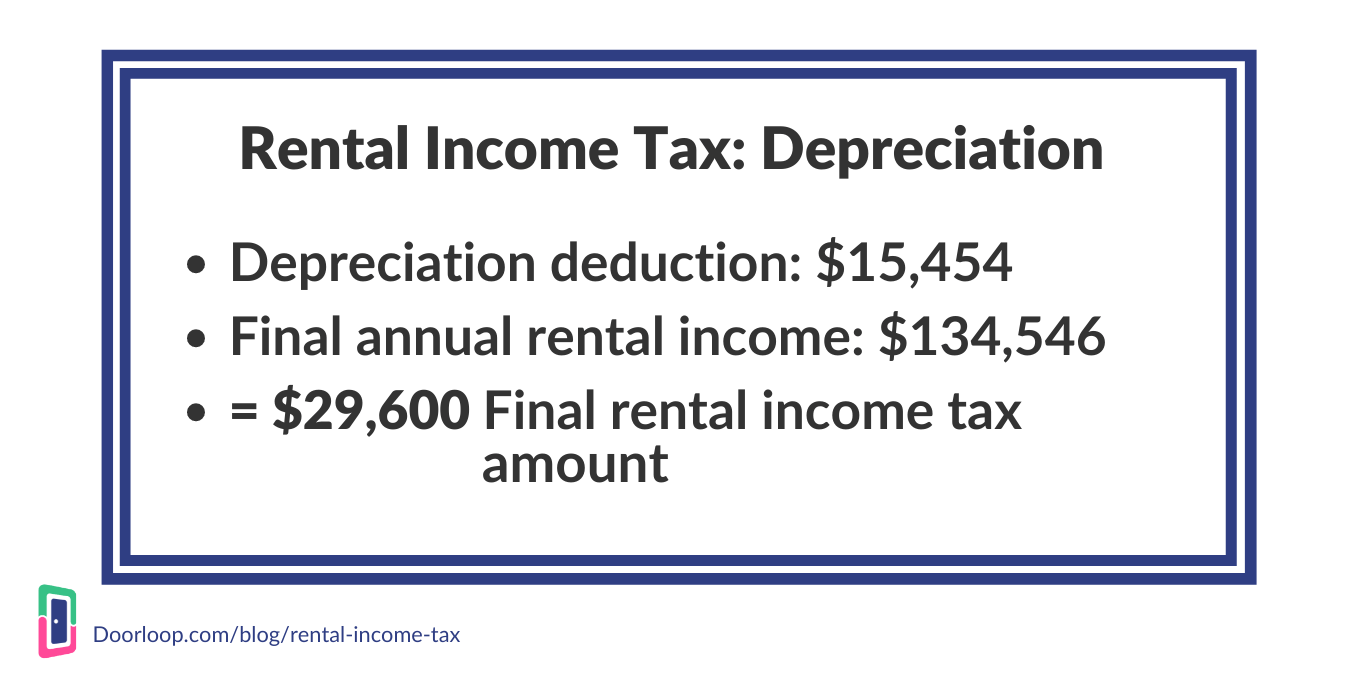

Remember that for depreciation, residential properties are divided by an estimated 27.5-year lifespan.

First, we subtract the $50,000 lot value, which is $425,000.

Then, $425,000 divided by 27.5 equals: $15,454.

So, once again we have a nice chunk to deduct from our taxable rental income.

Our $150,000 of taxable rental income minus the $15,454 then becomes $134,546.

Running our 22% tax bracket calculation once again, we end up at now just $29,600 in rental income tax, a far cry from our original $47,520.

Use these tips to be ready come tax time

Did these tips and examples help you figure out how to optimize your rental income on paper in a way that reduces your tax burden?

We hope so!

There’s a good chance that– between the many deductions and other opportunities– there’s something else you can do to reduce the amount of rental income tax you’re paying.

Even if you were already deducting basic expenses.

Managing all your property accounting– not to mention everything else you need to do to manage your properties– can be tough.

That’s why we’re so passionate about DoorLoop.

With DoorLoop, you can manage all your property accounting in one place.

You can collect rent through a convenient tenant portal, sync accounts, reconcile easily, manage your entire chart of accounts, and much more.

Did we mention that you can do all your property management from within DoorLoop?

From your smartphone?

How about:

- Simplifying maintenance management

- Automating certain marketing tasks

- Streamlining the leasing process

- Funneling multiple communications channels into one easy to manage platform

- And more

“Thanks, those property management tools sound great, but I’m pretty set for my accounting with QuickBooks,” you say?

We understand, that’s why we also have a super convenient QuickBooks Online integration.

It allows you to sync your QuickBooks account with DoorLoop seamlessly, so you can manage your properties with DoorLoop while continuing to do your accounting through QuickBooks.

(And have them place nice with each other, too.)

Frequently Asked Questions