Key Takeaways

- A 1031 exchange lets multifamily owners defer capital gains taxes while moving capital into properties that better fit market conditions, maintenance goals, or growth plans.

- Full tax deferral generally requires like-kind investment real estate, the same taxpayer, and replacement property and debt equal to or greater than what you sold.

- The 45-day identification deadline and 180-day closing deadline drive the exchange, so line up candidates and a qualified intermediary before closing.

- Boot is taxable immediately, including reductions in value or mortgage debt, so model fees, loan balances, and replacement values before committing.

- Vacation-home conversions, residence swaps, tenancy-in-common deals, and estate planning can work, but operators should document rental use and report exchanges on IRS Form 8824.

Looking to take advantage of 1031 exchange rules for one of the properties you’re managing?

Or maybe you’re a seasoned property manager or real estate investors who know the ins and outs, but are looking for info on exceptional use cases, such as vacation homes.

In this guide, you’ll learn everything there is to know about 1031 exchanges and IRS 1031 exchange rules.

Need to skip ahead to something specific? Just click from the table of contents below:

If you’re new to 1031 exchanges, let’s start from the top.

What is a 1031 exchange, how do they work, and what are the benefits?

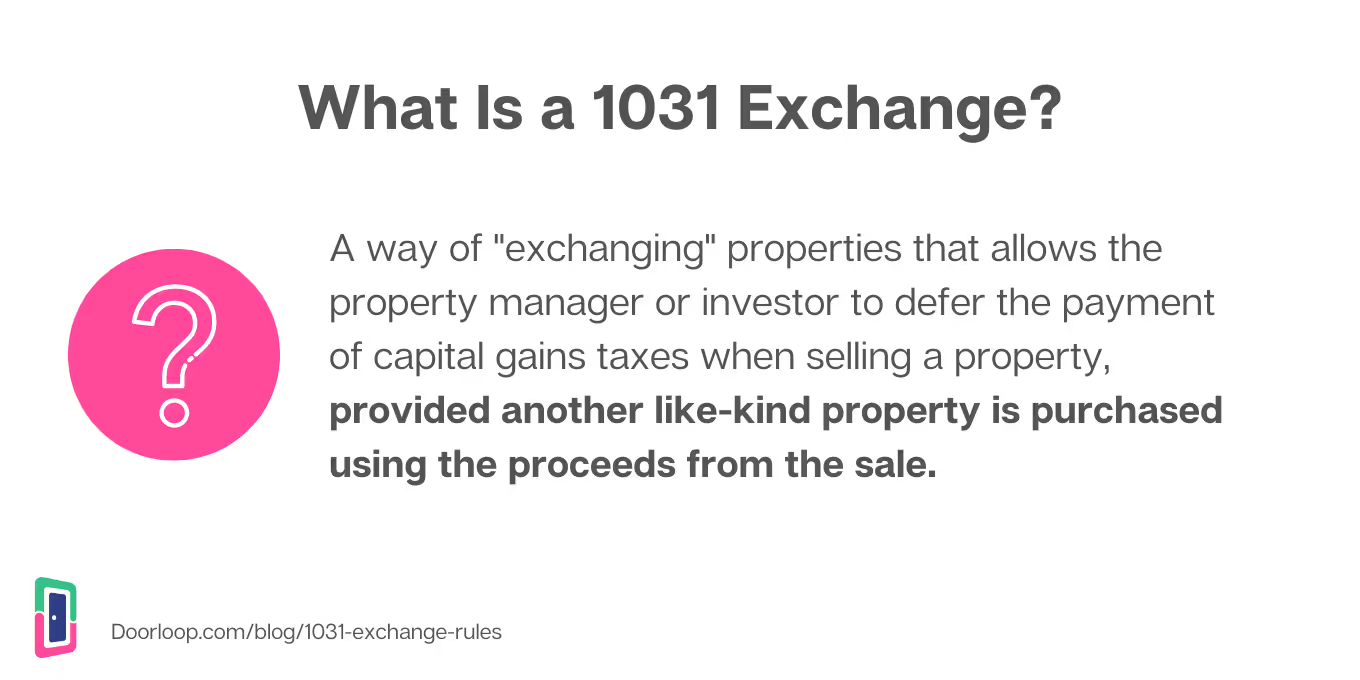

What is a 1031 exchange?

A 1031 exchange, or “like-kind” exchange, is a method of exchanging investment properties that allows you to defer capital gains taxes.

Referred to by its namesake, IRS Code Section 1031, the bill was passed in 1921 to encourage active reinvestment by giving an investment real estate investor the ability to avoid taxation of ongoing investment property.

What are the benefits of a 1031 exchange?

The primary benefit of a 1031 exchange is the obvious tax deferment.

With a 1031 exchange, you can defer taxes on the investment properties you own or manage indefinitely until you sell, exchanging from one property to another.

This is particularly advantageous when you consider what this allows you to do, and it opens up a whole collection of added benefits.

Such as:

1. Exchange for market conditions

For example, let’s say you’re worried about another bubble.

You can take some of your class C properties and exchange them for more stable class A, helping you weather the storm.

In the same way that a stock investor might shift investments from live stocks to the S&P, with a 1031 exchange, you’re able to move your capital gains taxes around in a way that minimizes your risk.

2. Exchange to minimize upkeep

Also, similarly, you could shift some of your class C or D properties to lower maintenance class A or B properties if the upkeep is too much.

3. Exchange to take advantage of a developing area

Or, you could shift your properties from one location to a more desirable or promising location in an effort to position your properties for greater future returns.

And the great part is, there is no limit to how often or how many exchanges you can do.

You can continue to shift your investment capital around to maximize returns and create your ideal portfolio.

1031 Exchange rules explained

A 1031 exchange is pretty straightforward.

If you own or manage investment or business property, you can exchange it with a like-kind property to defer capital gains tax.

If you follow the rules.

It’s important to understand 1031 exchange rules and requirements before doing one on any property you manage or own.

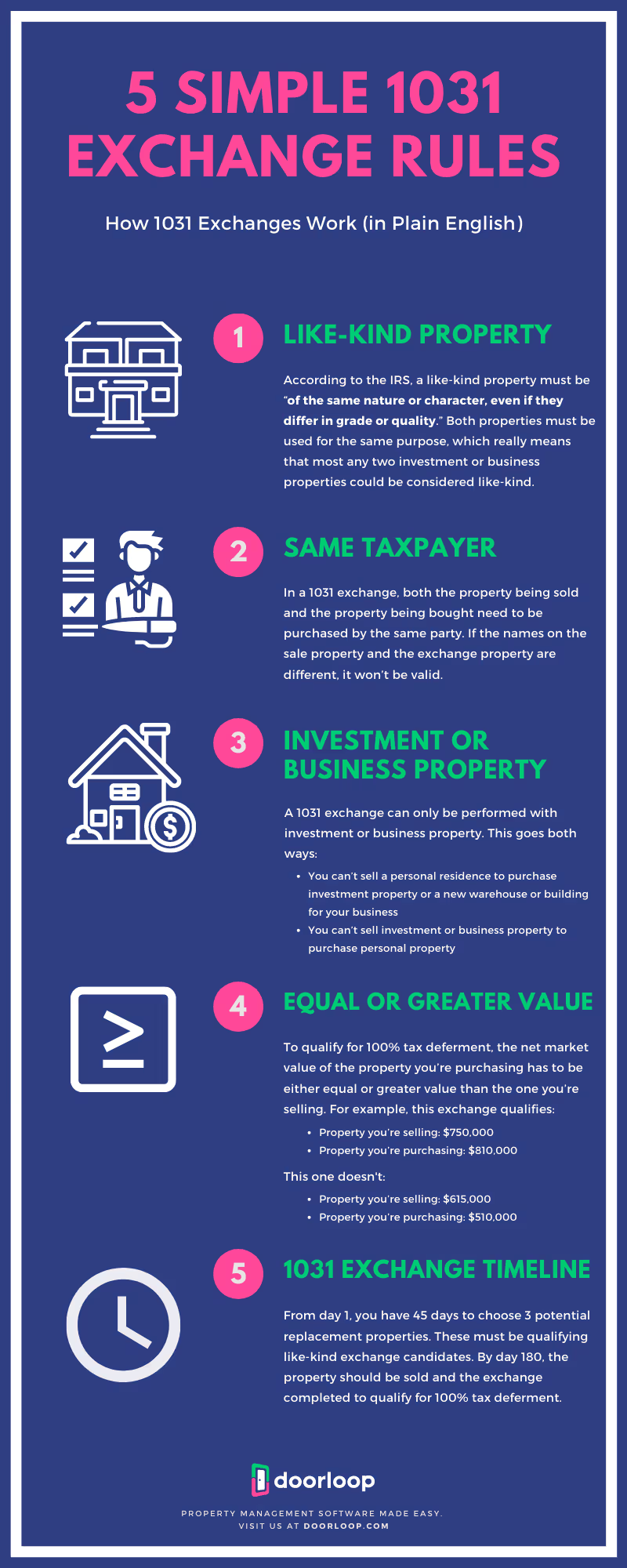

1031 exchange rules: At a glance

- Needs to be like-kind property

- Must be the same taxpayer

- Needs to be investment or business property

- Property must be of equal or greater value

- Must follow the 1031 exchange timeline

These are the same 1031 exchange rules for California, Texas, New York, or any of the other 50 states you might manage or own properties. So no matter where you are, these are important to know.

Each of these could use some explanation, so let’s break them down quickly:

1. Needs to be like-kind property

To do a 1031 exchange, the new property you’re purchasing needs to be “like-kind” the property you’re selling.

According to the IRS.gov website, a like-kind property must be “of the same nature or character, even if they differ in grade or quality.”

That’s pretty vague, but the rules are pretty generous.

Both properties must be used for the same purpose, which essentially means you can make a case that any two investment or business properties are like-kind.

You can even relinquish one property in exchange for two new properties in some cases.

For example, a rental in exchange for two commercial properties.

2. Needs to be the same taxpayer

This might be obvious, but it’s worth noting: in a 1031 exchange, both the property being sold/exchanged and the property being bought need to be purchased by the same party.

If the names on the sale property and the exchange property are different, it won’t be accepted.

3. Needs to be investment or business property

A 1031 exchange can only be performed with investment or business property.

There was previously a loophole that allowed the use of personal property in some cases, but due to recent changes with the 1031 exchange law, that’s no longer the case.

According to the IRS, “Under the Tax Cuts and Jobs Act, Section 1031 now applies only to exchanges of real property and not to exchanges of personal or intangible property.”

Keep in mind that this goes both ways:

- You can’t sell a personal residence to purchase investment property or a new warehouse or building for your business

- You can’t sell investment or business property to purchase personal property

4. Property must be of equal or greater value

This one isn’t a full requirement, but it will eat at your tax deferment and essentially nullify the whole purpose of the exchange.

To qualify for 100% tax deferment, the net market value of the property you’re purchasing has to be either equal or greater value than the one you’re selling.

For example, this exchange qualifies for 100% deferment:

- Property you’re selling: $750,000

- Property you’re purchasing: $810,000

But this one doesn’t:

- Property you’re selling: $615,000

- Property you’re purchasing: $510,000

It’s important to note that this applies to the mortgage as well.

Both the value of the property and the mortgage on the property you’re looking to purchase must be equal or greater than the value and the mortgage on the property you’re selling.

For example, this exchange qualifies for 100% deferment:

- Property you’re selling: $750,000 value, 500,000 mortgage

- Property you’re purchasing: $810,000, 650,000 mortgage

This doesn’t:

- Property you’re selling: $750,000 value, 500,000 mortgage

- Property you’re purchasing: $810,000, 450,000 mortgage

Remember: this is just to qualify for 100% tax deferment.

As we’ll touch on in the next 1031 exchange rule, you can qualify for an exchange even if the value or mortgage on the new property is less than the original for sale property.

Helpful note: fees such as broker and inspection fees apply here, so make sure to include them in your calculation for the most accurate estimate.

“Boot” (Or: What happens if the value of the property I’m buying is less than the one I’m selling?)

What is “boot”?

Boot is the difference in value between the property you’re selling/exchanging and the one you’re buying.

Remember what we mentioned a moment ago:

You can still qualify for an exchange if the value of the property you’re purchasing is less than the one you’re selling/exchanging.

So then, what happens if it is?

You pay capital gains tax immediately (at purchase) on the boot amount.

Let’s look at an example:

- Property you’re selling: $1,250,000

- Property you’re buying: $1,100,000

- Boot: $150,000

- Capital gains paid on: $150,000

- Capital gains deferred on: $1,100,000 of purchase value

5. Must follow the 1031 exchange timeline

One of the more confusing aspects of this whole process is the 1031 exchange timeline you have to perform the exchange.

So, let’s make it crystal clear.

From the moment you close on the for sale property, the timeline begins.

Day 1.

From day 1, you have 45 days to choose 3 potential replacement properties.

These must be qualifying like-kind exchange candidates.

Keep in mind: you’re not choosing one right now, you just need to have your 3 candidates selected.

What if you change your mind?

If you change your mind later and decide not to select one of your original 3 candidates, you’ll incur capital gains tax and essentially nullify the major benefit of the exchange.

So, be careful when choosing your exchange candidates.

What if I’m having trouble narrowing down my 3 candidates (Or: the 200% Rule)

There is one exception to this: the “200% rule”.

If you can’t decide between just 3 properties, you are allowed to select additional candidates.

The only 1031 exchange rule is this: the total value of those replacement candidates must not exceed 200% of the value of the original property which you sold.

Day 45.

OK, back to our timeline.

Now that you’ve selected your candidates, the final 135 days in the exchange timeline are reserved for finalizing the purchase of the new property.

By the end of the 180-day window, the exchange should be completed to qualify for 100% tax deferment.

Who qualifies to do a 1031 exchange?

So, who qualifies to do a 1031 exchange?

The qualifying parties are pretty all-inclusive. You can do a 1031 exchange if you’re a property investor or you simply own business property.

And you can perform a 1031 exchange if you’re an:

- Individual

- C corp

- S corp

- Partnership (general/limited)

- LLC

- Trust

- Or any other taxpaying entity

What property qualifies for a like-kind exchange?

Earlier, we touched on like-kind exchanges.

However, you might still be a bit unclear as to what exactly qualifies as a like-kind exchange.

So, let’s dive in a little deeper with some examples.

Like-kind property is defined as a property of the same:

- Nature

- Character, or

- Class

Note: Quality and grade don’t matter with regards to like-kind property.

For example, you can exchange a small office building for a small apartment complex, vacant land, or a larger office building.

All of those would qualify as like-kind exchanges because they need only be one of the same: nature, character, or class.

The one major exception to this, particularly for property managers of overseas investors, is that property outside the United States is never like-kind to U.S. property (which only makes sense, given that it’s a U.S. tax code).

Types of 1031 exchanges

There are 4 different kinds of 1031 exchanges:

- A deferred or “delayed” exchange

- Simultaneous exchange

- Reverse exchange, and

- Construction or improvement exchange

Let’s break each down and go over some pros and cons:

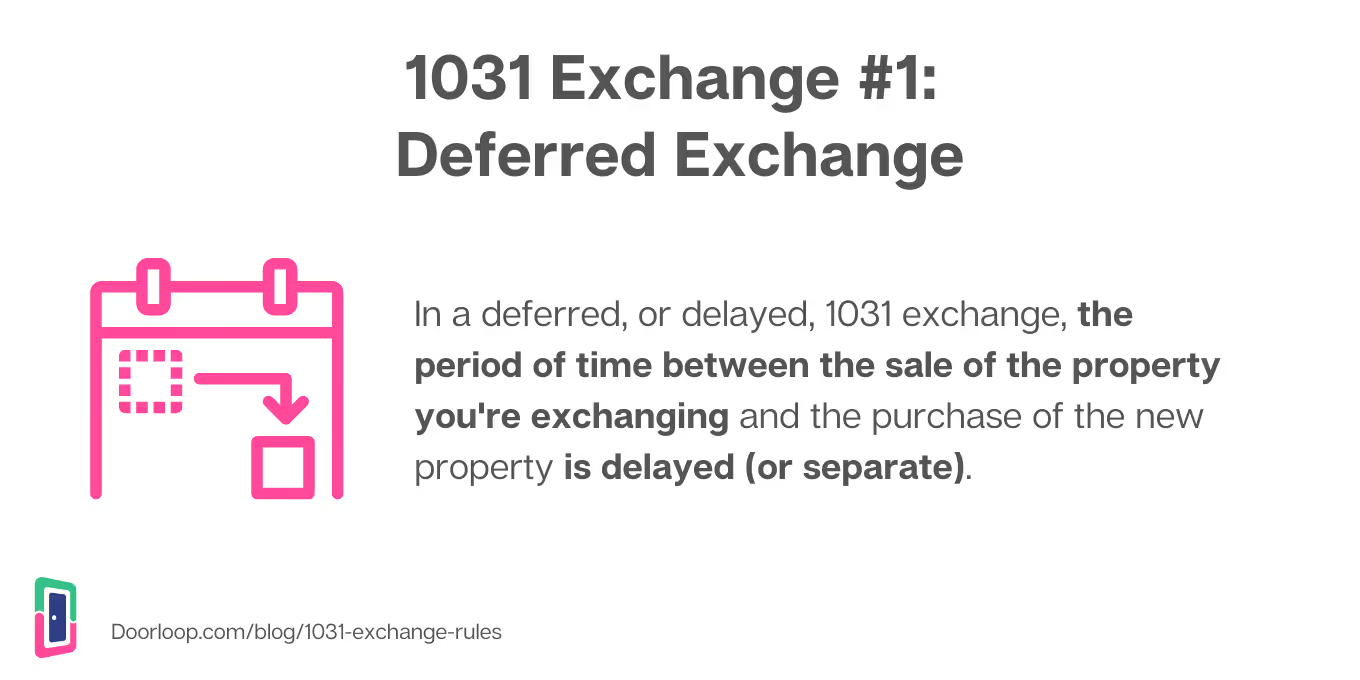

1. Deferred exchange

By far the most common type of 1031 exchange and the one most are familiar with.

In a deferred or delayed exchange, the time between the sale of your current property and the purchase of a new property are separate from one another.

Once the sale closes, you have 180 days in total to:

- Hire a qualified intermediary to initiate the sale and holds the funds in a trust to be used to purchase the like-kind property

- Select an exchange property

- Purchase the new property

2. Simultaneous exchange

In a simultaneous exchange, the property you’re selling (or exchanging) and the property you’re buying close on the exact same day.

As opposed to a deferred exchange, this one doesn’t offer much flexibility and can be difficult to pull off.

After all, even a small delay in the process on either side can throw everything off.

There are 3 ways a simultaneous exchange can be performed:

- Qualified intermediary: Here as well you can hire a qualified intermediary to handle the whole process, taking some of the stress off your back.

- Third-party exchange: A third party other than a qualified intermediary manages the process.

- Deed swap: An exchange of deeds (essentially a trade) happens with the other party, who is simultaneously purchasing your property and selling you one of theirs.

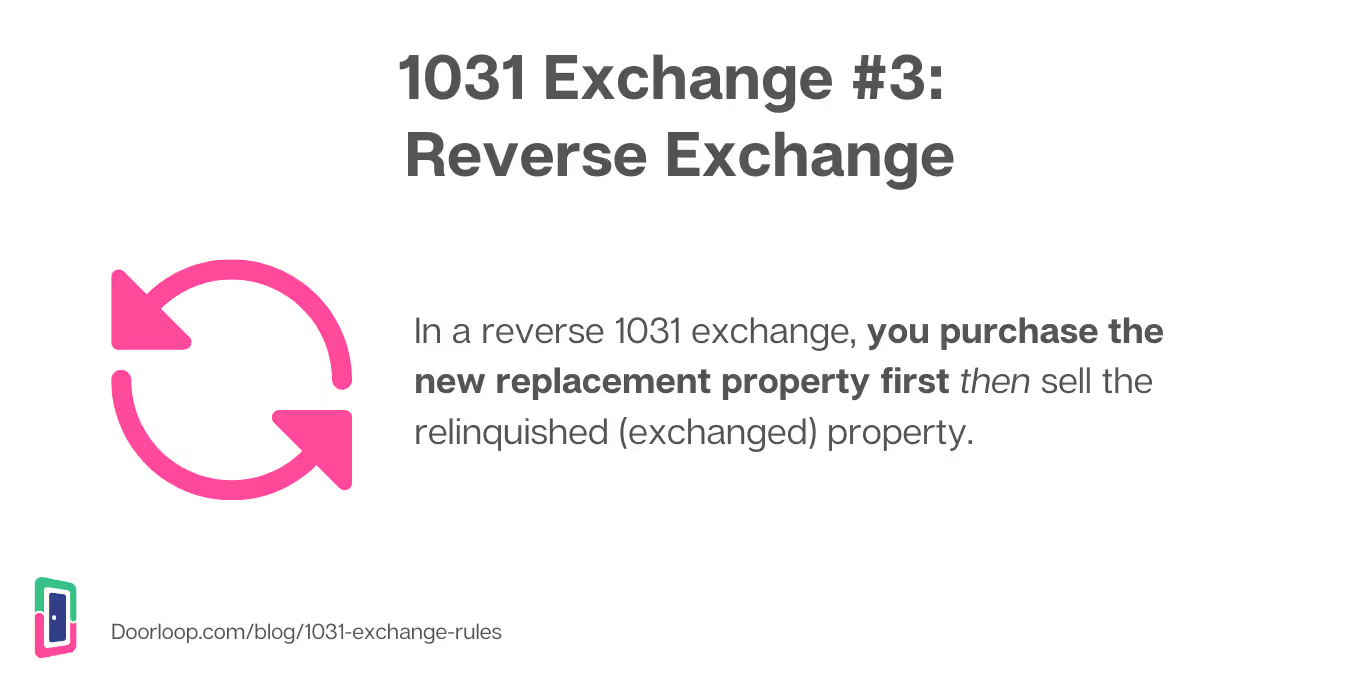

3. Reverse exchange

In a reverse or forward exchange, things are flipped on their head.

First, you purchase the new property. Then you sell the old (often referred to as) relinquished property.

Keep in mind: to do a reverse exchange, all cash is required for the purchase of the new property.

In this type of exchange, like the deferred exchange but the reverse, you have 180 days to sell the old relinquished property.

If you don’t, the exchange is canceled and you’re due for the tax liability.

Between the purchase of the new property and the sale of the old one, that property is “parked”.

Once the old property is sold, the proceeds are forwarded by your intermediary, typically through a trust, and the exchange is complete.

4. Construction exchange

In the final type of exchange, a construction or improvement exchange, you have the flexibility to perform improvements using the equity from the sale of the exchanged property.

The only caveat to that is that there are a few 1031 exchange rules you need to follow:

- All of the equity from the sale must be spent on improvements or as a down payment during the purchase of the new property by the 180th day of the exchange process

- You as the buyer must receive “substantially the same property” of that which you identified by the 45th day of the exchange process

- Improvements must be completed before the title can be transferred over to you

1031 & COVID

Many are now wondering how COVID has impacted 1031 exchange timelines.

On April 9th, 2020 the IRS published a notice (2020-23) intending to provide relief to taxpayers who had been affected by COVID.

Within that notice was included the extension of IRS 1031 exchange deadlines for 2020.

Both the 45-day selection period and 180-day exchange periods were extended to 120 days beyond the original due date.

This extension, however, ended on July 15th, 2020 and there are currently no further extensions announced by the IRS for 1031 exchanges or any new 1031 exchange rules.

We’ll keep this space updated for any further extensions or exceptions to be made aware of, COVID or otherwise.

Specific use cases

There are some special cases to be aware of when it comes to doing a 1031 exchange.

In most cases, they may not apply to you.

However, it’s worth making yourself aware of them in the rare event that one applies.

1031 exchanges and vacation homes

In the past, the law was more lenient in terms of what you could do with a vacation home via a 1031 exchange.

Since 2004, restrictions have been put in place. However, it’s still possible to turn a vacation home into a rental and then 1031 exchange it.

For example, let’s say you have a summer home that you’ve stopped using. So, you decide to transform it into a rental.

There are no exact time periods put in writing, but so long as you’ve had tenants in the property for at least 6 months, preferably a year, a 1031 exchange is generally considered safe.

The time with active tenants (not just up for rent, there should be tenants renting the property) is key, so the longer the better.

1031 swap residence

What if you decide that you’d like to convert one of your 1031 exchanged properties to your primary residence?

You can do it without incurring the wrath of your deferred capital gains tax, but there are caveats.

First, a 2008 IRS ruling set forth a safe harbor rule that states you must meet these two rules within each of the first two years immediately following the exchange for it to maintain its classification as an investment property:

- The unit must be rented to another person for a fair rental for a minimum of 14 days

- You cannot use the unit for personal use for the greater of 14 days or 10% of the number of days during the said 12-month period that the unit was rented out

In other words, it’s generally safest to rent out the property upon 1031 exchange for 2 years before converting it into your personal residence.

In addition to this, if you have any plans of selling that primary residence within 5 years of the exchange, you won’t be shielded by the primary-residence capital-gains tax break.

So, consider carefully what your plans are for the property, whether you plan on using it long-term (at least beyond 5 years) or later exchanging it or not.

Tenancy-in-common

Tenancy-in-common gives you the ability to invest and obtain fractional ownership in a much larger property, with up 35 total investors.

This offers several benefits, including:

- The ability to obtain a stake in a much larger investment property than you’d otherwise be able to obtain on your own

- The ability to diversify holdings

- Or consolidate those holdings

It’s important to note that when using tenancy-in-common, you have the same rights as a full owner.

That means you can sell your portion of the property at any time, so long as you can be accredited by meeting certain financial requirements.

How to report 1031 exchanges on taxes

IRS Form 8824 is used to report a 1031 exchange on your taxes.

Make sure to file it for the year the exchange occurred.

Some of the information you’ll need include:

- Dates when the property was identified and transferred

- Value of the property received

- Property descriptions

- Any possible relationship between the two parties involved in the exchange

- Cash received or paid

- Adjustable basis of like-kind property sold/relinquished

1031 exchanges and estate planning

One of the greatest long-term benefits of using 1031 exchanges in real estate investing is the ability to completely erase the deferred tax debt upon the inheritance of the property.

When a property is inherited through a 1031 exchange, meaning that property was acquired at some point in time through the use of a 1031 exchange, the value of the property is “upgraded” to fair market value and the tax debt is erased.

Make sure to consult an estate planner to make sure you are following the IRS 1031 exchange rules correctly and the right steps are put in place as there are details that can invalidate this process.

A useful tool for the property manager’s toolbelt

A 1031 exchange is a tool that should be used wisely.

After all, you don’t want to mess with the IRS.

However, when utilized properly, it can help elevate the performance of investment property and give incredible flexibility on multiple levels.

Just make sure to consult with a qualified intermediary before the process if it’s your first exchange to make sure you have all the right pieces in place.

Disclaimer

The materials and information available at this website and in this article are for informational purposes only and not for the purpose of providing tax or legal advice. You should contact your attorney and/or accountant to obtain advice with respect to any particular issue, question or problem.

And don’t forget to check out more of DoorLoop’s rental investing and property management content:

- Pros and Cons of Investing In Real Estate

- Active Vs. Passive Investing

- Important Questions Investors Should Ask Before Investing In Real Estate

FAQ

What are the IRS rules for a 1031 exchange?

These are the rules for a 1031 exchange at a glance:

- Needs to be like-kind property

- Must be the same taxpayer

- Needs to be investment or business property

- Property must be of equal or greater value

- Must follow the 1031 exchange timeline

How long do you have to hold a 1031 exchange property?

If a property has been acquired through a 1031 Exchange, it should be held for a minimum of five years.