Key Takeaways

- A clean chart of accounts is the foundation for scalable multifamily accounting, giving teams accurate profit and loss, cash flow, and rent roll reporting.

- Use rental ledgers for property-level income detail and rent rolls for portfolio-wide visibility into recent payments, balances due, and future rent.

- Treat rental income as ordinary income, but protect net income by tracking deductible expenses, depreciation, QBI, and entity-specific tax documents before filing season.

- Growing portfolios should move rent collection, bank syncing, reporting, and vacancy workflows out of spreadsheets and into property management software built for rental operations.

If you own rental property and you’ve been working to better manage your rental property finances, you’ve probably run into some pitfalls.

Not only are there multiple different types of rental income, but there are lots to consider when managing it.

For example:

- Where does it go? Do you need multiple accounts?

- How do you track your rental income properly?

- How do you handle taxes? The right way?

- And how do you keep all of them organized, especially when you get to the point of having dozens of properties?

A lot goes into managing rental property income, but there are some steps you can take now that will immediately make the whole process easier. Some you may not yet have in place.

Below, we’ll cover 5 major tips for how to manage your rental property income effectively.

Plus, some useful links and guides for tackling other important aspects of your rental property accounting and maximizing your ROI and rental income for those looking to bring their game to a whole different level.

How to Manage Rental Property Income: 5 Tips

Managing rental property income involves a lot of moving parts, but there are some clear best practices that will make things significantly easier.

Here are some tips for managing your rental property income right:

1. Have a clean chart of accounts that allows you to map out all your accounting items

A chart of accounts– whether you’re a landlord with one property, a few hundred properties, or a prop management team– should serve as the foundation of your entire property accounting.

It’s from here that you’re able to pull key reports to find out things like:

- What you owe and are owed, i.e. profit & loss

- As well as the coveted rent roll report that allows you to see key information for all your properties at a glance.

Without a chart of accounts, you can’t get a read on your portfolio’s cash flow or anything else for that matter.

To learn how to set up your chart of accounts, check out our guide: Property Management Chart of Accounts.

It includes a free sample template you can use to start creating your chart of accounts along with additional resources to make the whole process easier.

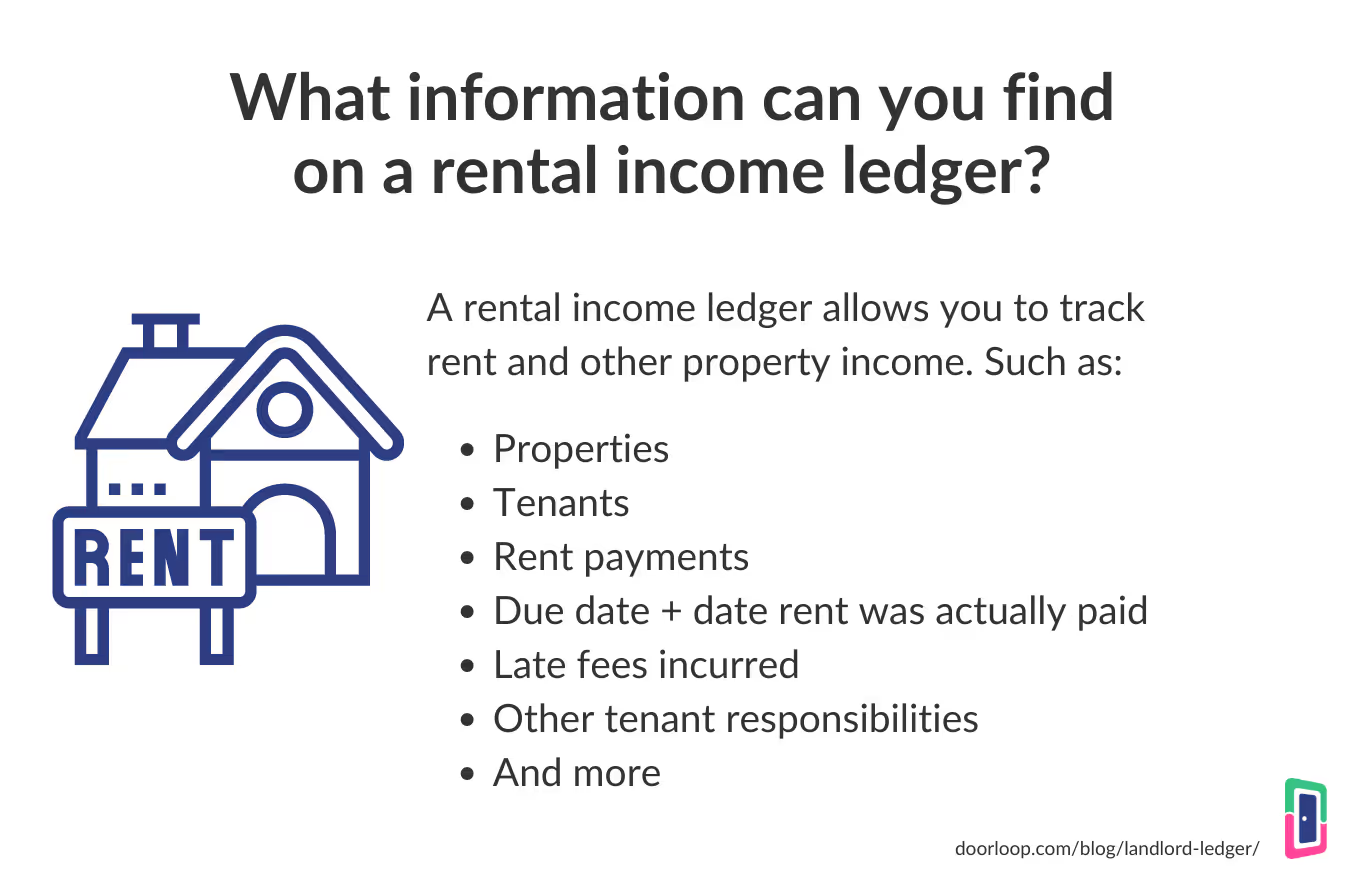

2. Set up your rental ledger and rent roll to get a clear picture of your rental income

Once you have your chart of accounts set up, you’re able to start running valuable reports like the ones we touched on above.

Two of the most useful are a rental ledger and a rent roll.

A rental ledger typically includes details about a single property, whereas a rent roll is a report with details regarding rental income for your entire portfolio including:

- recent payments

- How much you’re owed

- And future rent payments

The great news is, if you used a good property management tool like DoorLoop, these are created for you automatically.

It’s a simple matter of running and printing the reports for regular use.

Learn more about how to create your own rental reports in this guide: How to Create Your Own Rental Income Ledger.

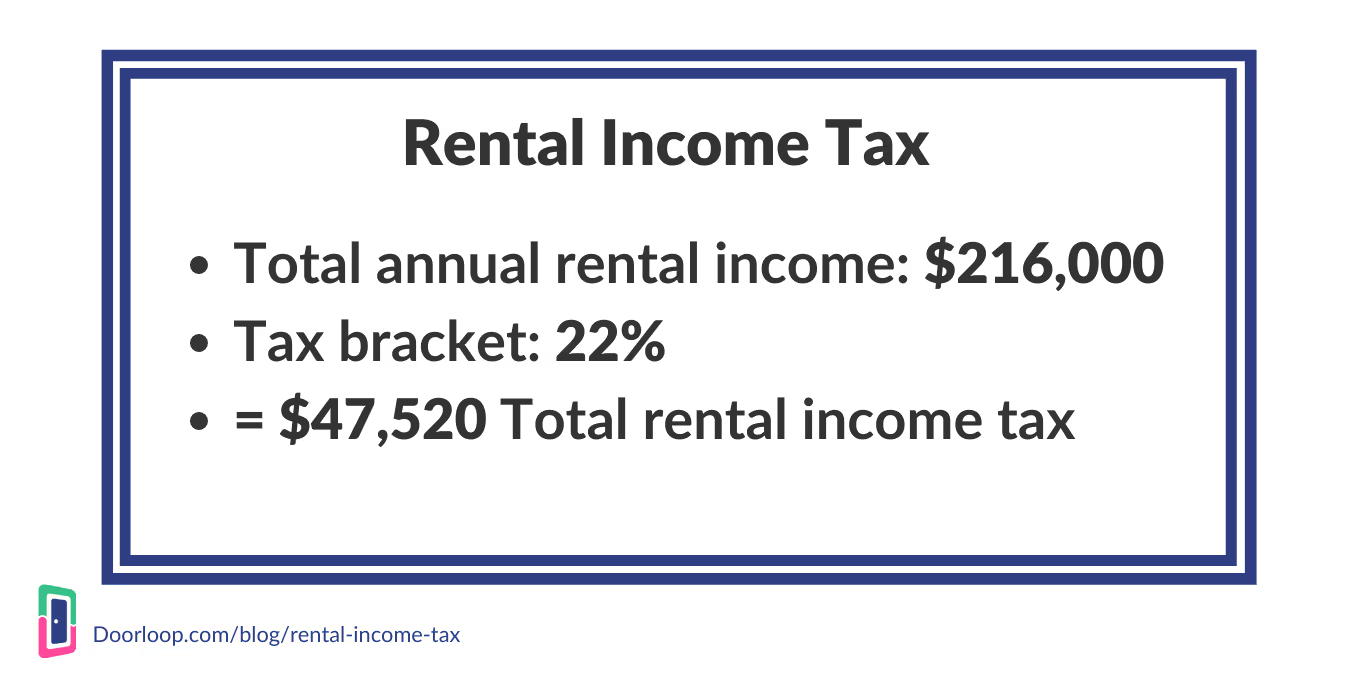

3. Learn how rental income tax works + how to reduce your tax burden

Rental income is taxed exactly like ordinary income you’d get from any 9-5 job or business if you’ve ever been a sole proprietor.

The big difference is in what is considered rental income and what you can deduct (and steps you can take) to reduce your rental income tax burden.

According to the IRS, rental income is “any payment you receive for the use or occupation of property.”

That includes:

- Security deposit funds retained (and only those retained)

- Monthly rent payments

- Other tenant services

- Premature lease cancellation payments

And how do you reduce your rental income tax burden?

How to reduce your tax burden

There are a few ways to do that, the most common of which involves taking as many deductions as possible.

Some of the more common items you can deduct include:

- Insurance premiums

- Repairs and maintenance

- Property tax

- And operating expenses

There are a few other potential deductions as well, which can be much larger.

Including:

- Depreciation on depreciable items

- And the Qualified Business Income deduction or QBI

For more tips on how to reduce your rental property income tax burden as well as how to calculate it, check out our guide: How Rental Income Tax Works (+ Tips for Reducing Tax Burden).

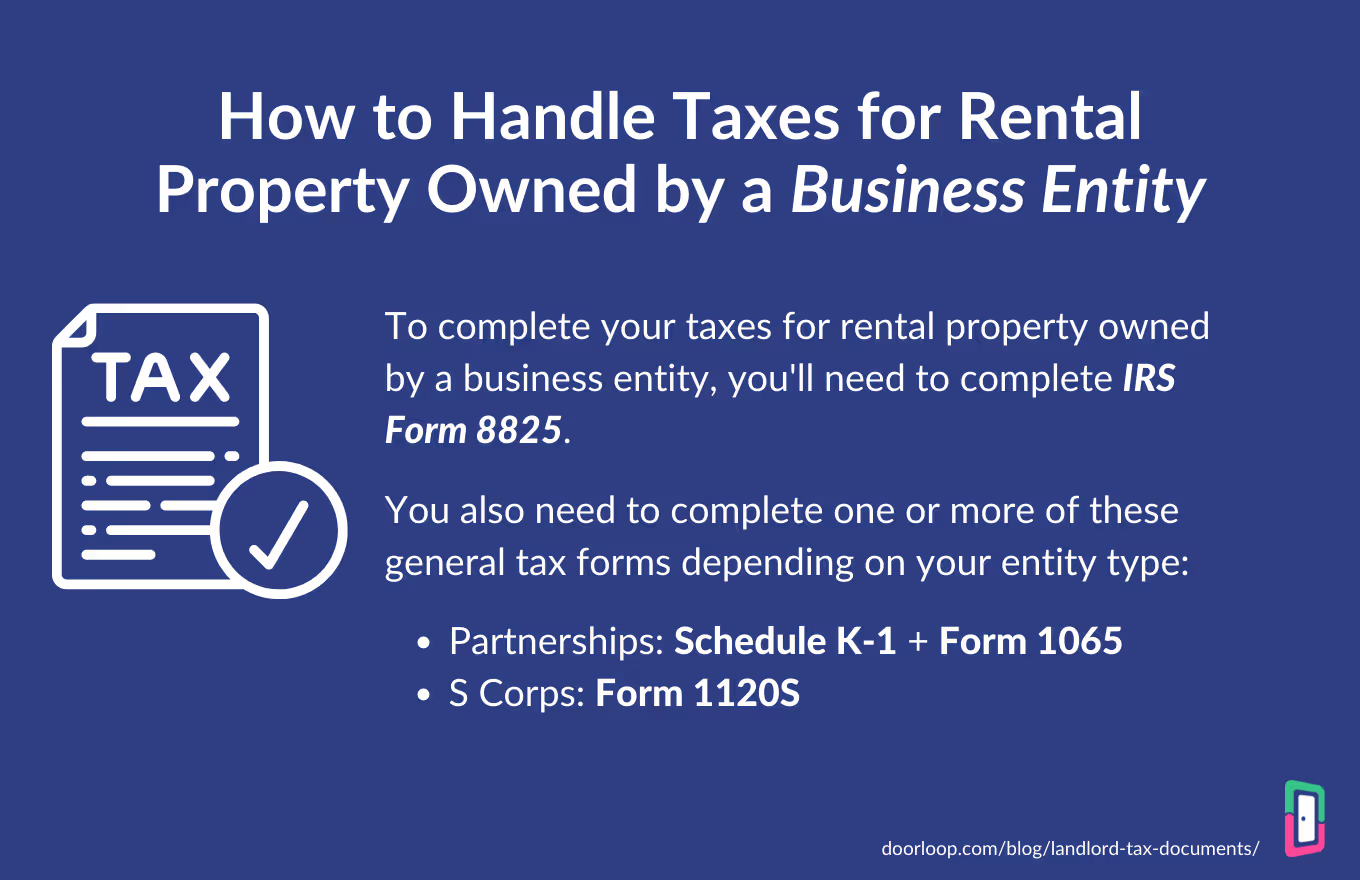

4. Gather your tax documentation now to maximize your tax savings and your net rental income

Another important step related to minimizing your tax burden and maximizing your net rental property income is to get your tax documentation in order.

Come tax time, if you don’t have your documentation in order, you could be looking at a very difficult time.

Not to mention, potential fines if you don’t submit everything on time.

But beyond that, you could end up paying more taxes than you should.

If your information isn’t correct, you could end up losing out on a key deduction you otherwise could have claimed on your taxes for that year.

Related to documentation, how you handle things all depends on what kind of business entity you have your property under. Such as:

- Sole proprietorship

- LLC

- Partnership

- S Corp

Learn more about taxation for rental properties based on the business entity in our guide: Landlord Tax Documents: Everything You Need to Know.

5. Use property accounting software to automate monthly rent collection

Whether you knew already or are starting to see it now, it should be clear that a lot goes into managing rental property income and property accounting in general.

Speaking of, managing all your rent payments in Excel spreadsheets isn’t super effective or efficient.

Fortunately, you can get access to tools now that allow you to simplify and streamline the whole process.

That's especially relevant for rental property owners, as early tools like QuickBooks aren't built for rental property income.

With prop management software, you can even automate and semi-automate several tasks as well depending on the software, such as:

- Collecting monthly rent

- Syncing bank accounts

- And putting up new listings when you have a vacancy

DoorLoop can help you streamline your entire property accounting. Schedule a free demo to find out what it can do for you.

Managing your rental property income becomes so much easier when using software.

Countless data points that once needed to be recorded manually are now done automatically the moment they happen.

It can require a small leap of trust to move to software if you’re used to having your hands on everything (i.e. inputting manually on a notepad or spreadsheet).

However, if your portfolio is growing and you’re in need of help managing it all, once set up you’ll wonder how you ever did it any other way.

Other best practices for managing rental property income

We covered a lot throughout this guide, but when it comes to property accounting, we really just scratched the surface.

If you’re looking to take your accounting to another level, dive into our complete master guide on property accounting, where you’ll learn:

- How to set up the accounting system for your rental properties

- Property accounting best practices

- Important terms and definitions

- 1031 exchanges

- And much more

Check it out here: Property Management Accounting: A Complete Starter Guide.

What is a good net income for rental properties?

The ROI you’re seeing for your rental properties and portfolio as a whole can vary wildly depending on a number of factors, including:

- The type of property

- Number of occupancies

- Repair costs

- The area, and

- Other factors

It’s generally agreed that a healthy number is somewhere around 7-10%, but you should calculate and shoot for above that.

However, keep in mind that this changes a bit depending on if you're talking about property management companies vs. a solo property owner/manager.

A company may be able to get by with a lower net income because they have a larger portfolio, while someone with just a few dozen properties might need to take every percent they can get just to break a decent profit.

It also depends on the area, as one market might be surging and bringing in a huge ROI while another market is barely scraping by.

Manage your rental property accounting right with DoorLoop

Being a property manager as a whole is a major effort.

But with these tips and the help DoorLoop’s all-in-one property management software, you can streamline and simplify the entire process.

Whether it’s:

- Automating your monthly rent collection, security deposits, or any other fee

- Getting easy access to a complete chart of accounts

- Robust reporting such as your rent roll report to keep track of your rental expenses

- Syncing your bank accounts seamlessly

- And even easy integration with QuickBooks Online

DoorLoop has you covered.

Schedule a free demo today to start taking your property accounting to a new level.