Key Takeaways

- Multifamily owners filing rental property under their own name, sole proprietorship, co-ownership, or single-member LLC generally report income and expenses on Schedule E.

- Entity-owned portfolios, including partnerships, S corps, multi-member LLCs, and limited partnerships, use Form 8825 plus entity-specific returns such as Form 1065, Schedule K-1, or Form 1120S.

- Co-ownership changes reporting: spouses with joint ownership use one Schedule E, while non-spouse co-owners each report income based on their ownership share.

- Tax planning should cover ordinary deductions, the QBI deduction of up to 20% for qualifying pass-through income, and residential depreciation over 27.5 years.

As a landlord, it’s easy to focus on the promise of recurring rental income and the other benefits of owning rental property.

But managing rental property, whether your own properties or those of your clients as a property manager, has certain responsibilities as well.

One of the biggest is handling your annual taxes.

Just the thought– taxes– *shiver* might make your eyes start to roll into the back of your head, but it’s not as difficult as it might seem to prepare your taxes for a rental property.

The main thing you need to know is that it all depends on if you’re filing as an individual or business entity as that will dictate what forms you need.

Once you know that, getting the right landlord tax documents in order is a simple matter.

Let’s start with what tax documents you need if you’re filing as an individual.

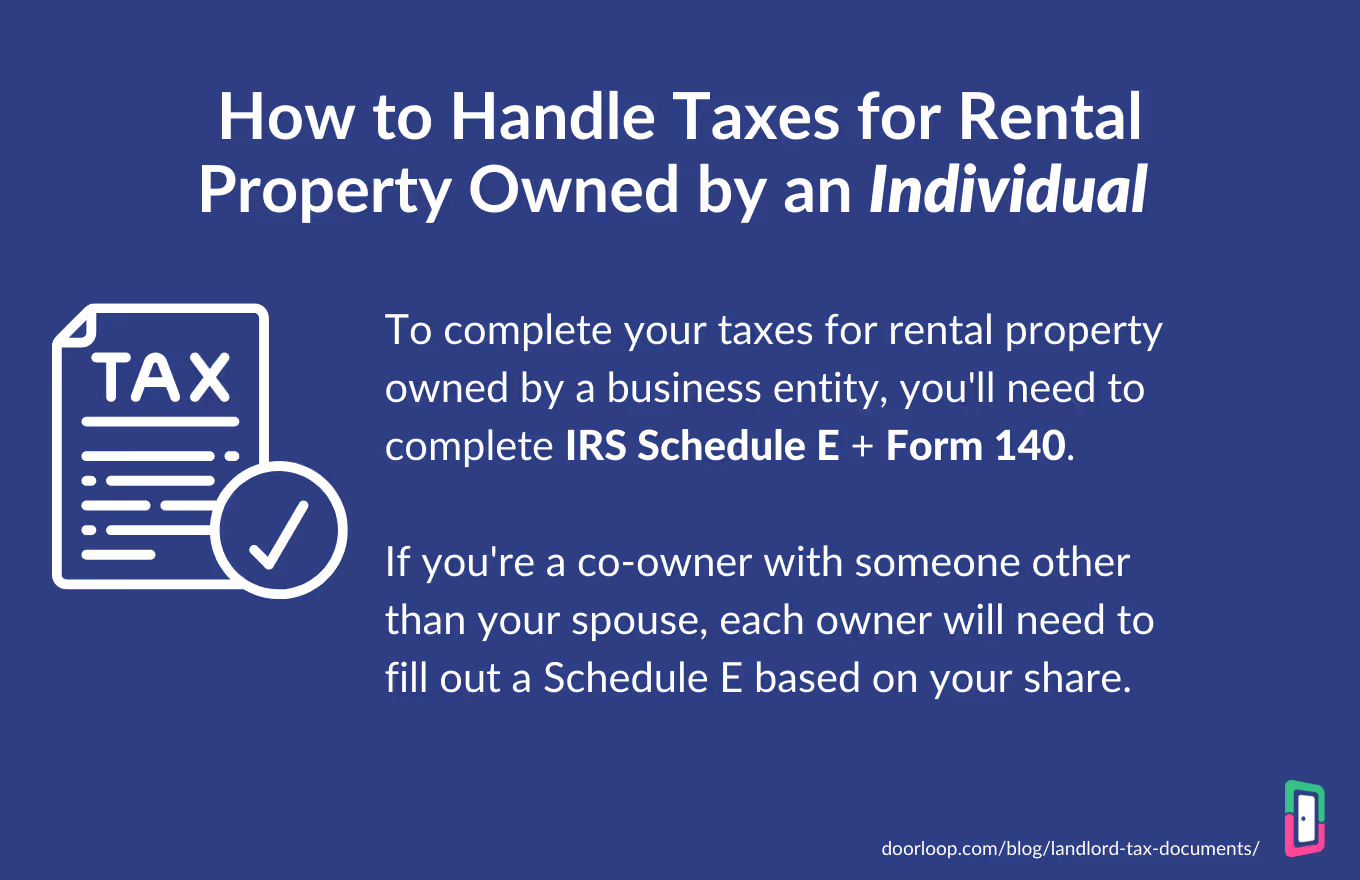

Schedule E (Form 1040)

This first section refers to those who are reporting rental property whose title is in their own name.

This includes:

- Sole proprietorships

- Co-ownership

- LLC (owned by a single person)

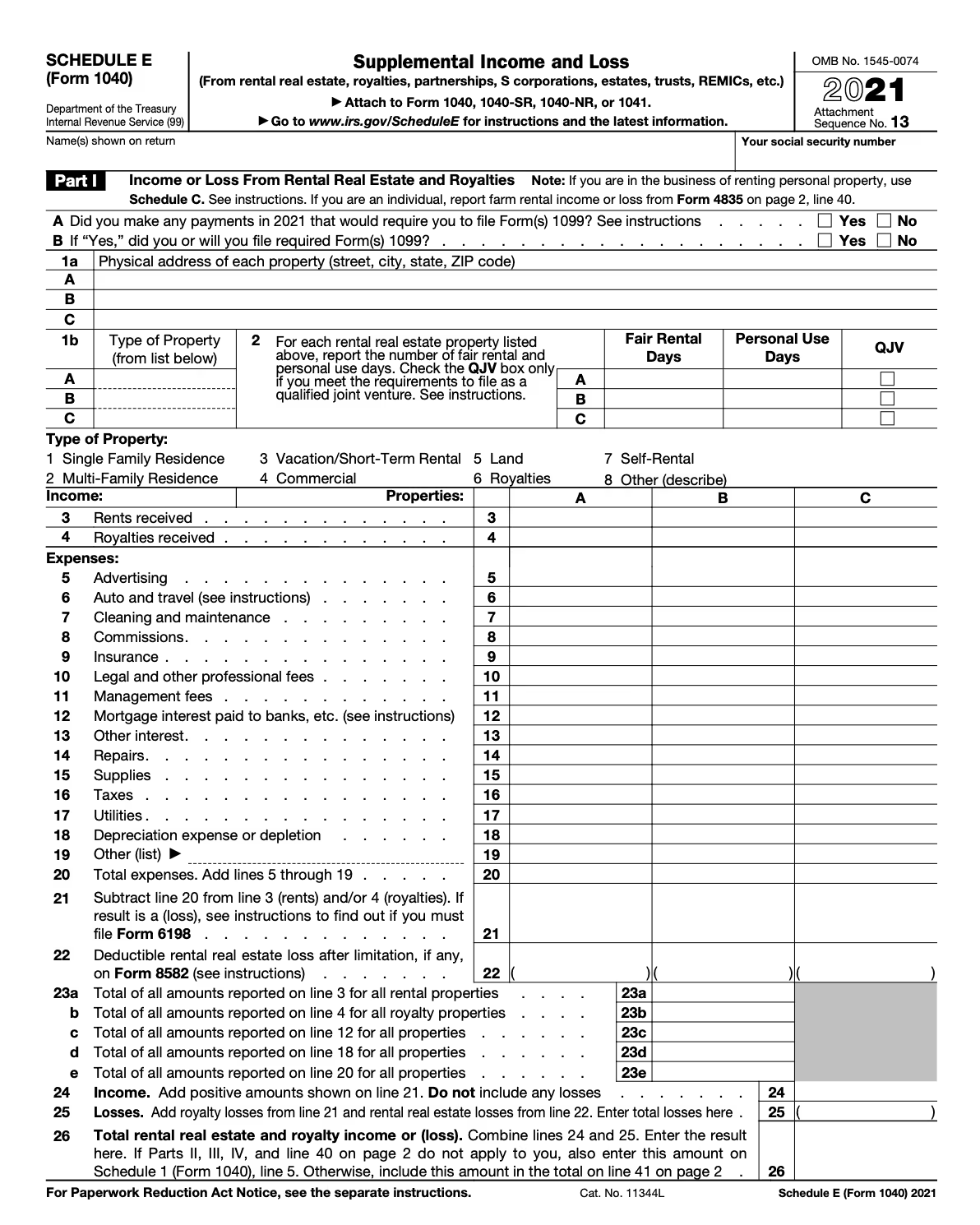

If that applies to you, you’ll need to submit IRS Schedule E (Form 1040), Supplemental Income and Loss.

The form is used to report both property-related income and expenses for that year.

Any profits obtained should be added to your total personal income, while likewise losses can be deducted from it in many cases.

Keep in mind that there are exceptions to virtually everything here, so it’s important to work with a professional if possible to make sure you’ve got everything inputted correctly.

A note on co-ownership

Co-ownership works a bit differently, but it’s pretty straightforward.

However, co-ownership is treated slightly differently depending on if you co-own with your spouse or someone else.

If you co-own with your spouse and you jointly own the property or properties, you need to report your rental income and expenses on a single Schedule E.

If you co-own with someone else that is not your spouse, yourself and your co-owners must each report your share of rental income on a separate Schedule E.

How much you report is based on how much of the property you own, so it’s pretty straightforward.

That means if you own 60% of a property, you’ll report 60% of the rental income on your Schedule E while your partner will report the 40% they own.

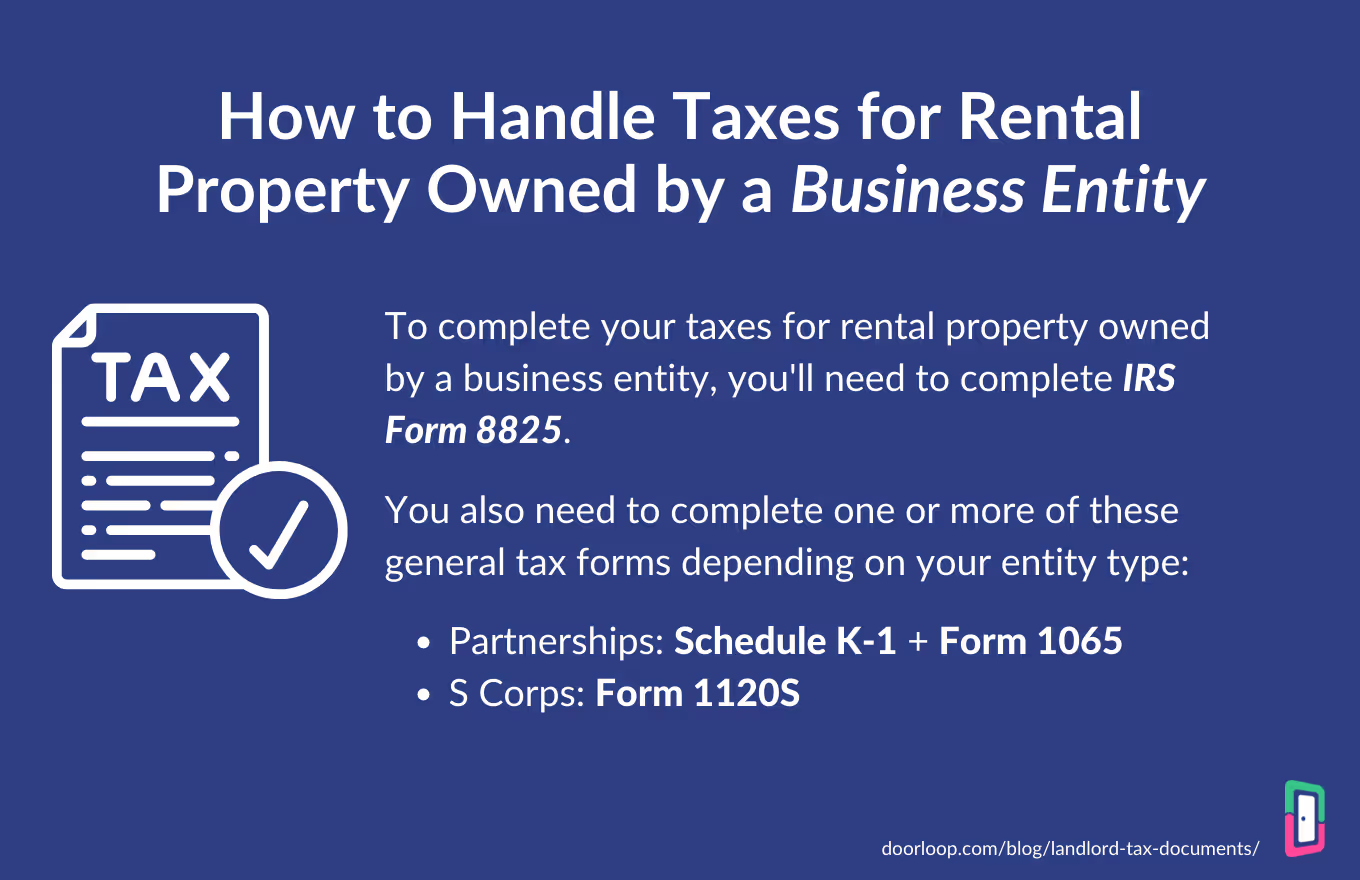

Rental income tax documents for business entities

Now, let’s talk about filing taxes for rental income when the property or properties are owned by a business entity.

That includes:

- S Corps

- Partnership

- LLC (with two or more members)

- Limited partnership

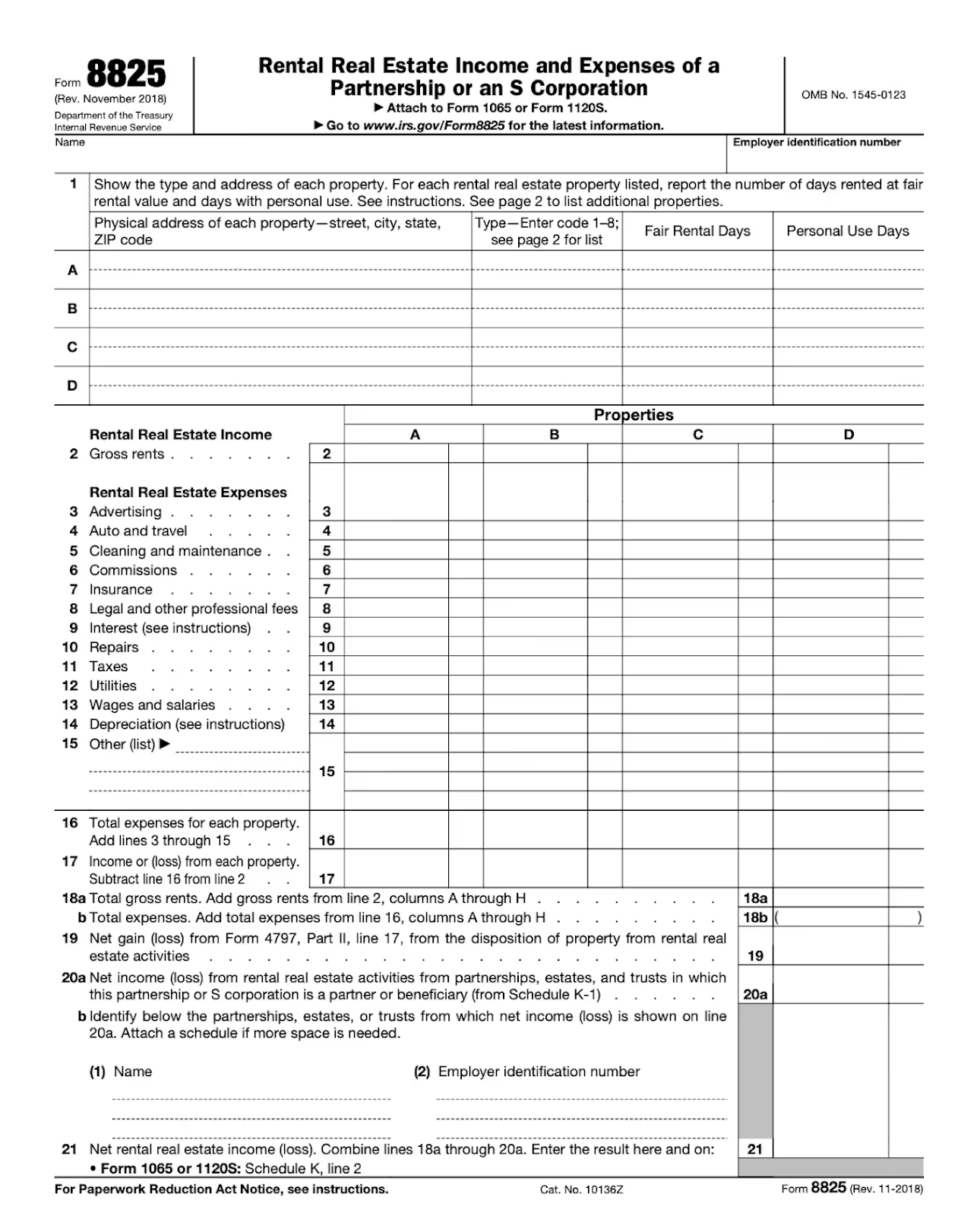

If that fits you, then you’ll fill IRS Form 8825, Rental Real Estate Income and Expenses of a Partnership or an S Corporation, to report your rental income expenses for the entity.

This is in addition to other tax documents you need to complete depending on your entity type.

Partnerships: Additional tax documents

Partnerships also need to submit these additional tax documents:

- Form 1065: This is to report activity from your business operations including revenue, expenses, and gains & losses.

- Schedule K-1: This is used to report net profit and losses attached to each owner’s interest in the company.

- Schedule E + Form 1040: Second page of Schedule E only in this case, as the first is strictly for individuals reporting rental income as we covered in the previous section.

S Corps: Additional tax documents

S Corporations also need to submit these tax documents:

- Form 1120S: Submit this to report profit or losses according to each shareholder.

- Schedule E + Form 1040: Second page of Schedule E only in this case, as the first is strictly for individuals reporting rental income as we covered in the previous section.

How to reduce your tax burden

So far, you know exactly what tax documents you need as a landlord or property manager to report your rental income and expenses.

Next, let’s talk now about ways to reduce your tax burden as a landlord.

1. Grab every straight tax deduction you can get

First, let’s talk about basic deductions.

There are some more complex deductions like depreciation, but we’ll talk about that later as it deserves its own point.

You can claim all kinds of deductions on your taxes to reduce your rental income tax burden.

Just some of those potential deductions include:

- Insurance

- Property tax

- Advertising expenses

- Interest

- Maintenance costs

This is just a small list of some of the most common deductions, however.

For more about what you can deduct see the IRS’s official documentation on potential deductions here: Tangible Property Final Regulations.

2. For those with property owned by a business entity: Qualified Business Income deduction

This one is a tip specifically for property owned by business entities such as S Corps and partnerships.

So, what is the Qualified Business Income deduction?

The QBI deduction allows you to deduct up to a whopping 20% (with a $163,000 individual cap) of your pass-through business income.

If you’re familiar with how corporations work, pass-through income is what it sounds like: any income generated from a pass-through entity.

It does have its limits, but the amount of income you can deduct in this way is high.

Individual taxpayers can deduct up to $163,000 while married taxpayers can deduct $326,600

It’s worth noting, however, that you can still claim a partial deduction if your pass-through income is above this level.

Read more at the official IRS page on the QBI deduction: Qualified Business Income Deduction.

3. Calculate and deduct depreciation

While technically another deduction, depreciation is unique among them for a few reasons and a big potential deduction, so let’s focus in on it for a sec.

You have the ability to deduct part of the value each year of larger business-related purchases.

For example, if you purchase a set of new laptops for your team for a total of $8,000 you can deduct a good portion of that on your taxes each year for every year of its “useful life”.

If you estimate that these laptops have a useful life of say, five years, you can deduct 20% of they’re value each year for five years.

That equals $2,000 of tax deductions each year for five straight years.

This gets extra sweet when you consider that property also qualifies under this rule.

According to IRS rules, this is the useful life of residential and commercial property, which use different timespans:

- Residential: 27.5 years

- Commercial: 39 years

If you own a residential property, you simply subtract the value of the land from the cost of acquiring the property and divide it by 27.5 to find out how much you can deduct that year.

Find out more about how depreciation deductions work at the IRS.gov here: Publication 946 (2020), How To Depreciate Property.

Additional resources for landlords and property managers

If you’re looking for more valuable resources related to everything property management, rental property taxes, and more, check out our other free resources:

- How Rental Income Tax Works (+ Tips for Reducing Tax Burden)

- 10 Landlord Documents and Forms (Free Template Downloads)

- Master resource: Real Estate Rental Form Templates

- How to Manage Property Taxes

- How to Refinance A Rental Property

Frequently Asked Questions