How to Manage & Calculate Property Tax?

If there’s one thing in this world that everyone has in common, it’s paying taxes.

This is especially true for landlords who have a rental property (unfortunately).

While it's not a whole lot of fun, it is important to know as much as possible about the taxes you pay on your property and to make sure that everything is being paid accordingly.

To help you do that, we’ve broken it all down into a comprehensive guide with everything you ever need to know.

To begin, let’s start with the different types of property-related taxes.

What are Rental Property Taxes?

As a landlord, it's important to understand the various taxes you may encounter when renting out a property.

In very simple terms, your rental income is taxed just like ordinary income, but with other, more complicated, rules.

This section will provide an overview of the different types of taxes landlords may encounter, as well as explain how rental property taxes are calculated.

What are the Different Types of Rental Property Taxes?

Below, we have outlined the common types of rental property taxes, as well as some important aspects of each one.

Property Taxes

Property taxes are taxes that are assessed on real property, such as rental property. These taxes are typically based on the value of the property and are collected by local governments.

The amount of property tax you will pay will depend on the value of the property and the tax rate in your area.

Rental Income Tax

In addition to property taxes, landlords may also be subject to income taxes on rental income. Landlords must report rental income on their federal tax forms since it is considered taxable income.

The amount of income tax you will owe will depend on your marginal tax rate and the amount of rental income you earn.

Also, this rental income applies to various types of rental income, including normal rent payments, advance rent, security deposits, and fees.

How to Calculate Rental Property Taxes?

In this section, we’re going to go over some of the ways that different kinds of real estate taxes are calculated, as well as some deductions and exemptions.

Sales Taxes

In some states, landlords may also be subject to sales taxes on the rental of their property.

Sales taxes are typically calculated as a percentage of the rental income and are collected by the state government.

The amount of sales tax you will pay will depend on the sales tax rate in your state and the amount of rental income you earn.

Taxable Income

To calculate the amount of rental property taxes you will owe, you will need to determine your taxable income.

Taxable income is calculated by taking your gross rental income and subtracting any allowable deductions and exemptions.

Allowable deductions may include things like property repairs, advertising expenses, and property management fees.

Deductions and Exemptions

As a landlord, you may be eligible for certain deductions and exemptions that can reduce the amount of rental property taxes you owe.

For example, landlords who own and occupy a residential rental property as their primary residence may be eligible for a homestead exemption, which can reduce their property taxes.

Additionally, landlords may be able to deduct certain expenses, such as property repairs and advertising expenses, from their taxable income.

How Is Rental Income Taxed?

Calculating rental income tax can be very difficult, especially because of all the different factors that need to be considered.

To estimate and budget for rental property taxes, landlords will need to consider the following factors:

- Property taxes: Landlords will need to research the property tax rate in their area and estimate the amount of property taxes they will owe based on the value of the property.

- Income taxes: Landlords will need to estimate the amount of rental income they will earn and calculate their marginal tax rate to determine the amount of income taxes they will owe.

- Sales taxes: Landlords will need to research the sales tax rate in their state and estimate the amount of sales taxes they will owe based on the amount of rental income they earn.

- Deductions and exemptions: Landlords will need to research the deductions and exemptions they may be eligible for and estimate the amount of tax savings they will receive from these deductions and exemptions.

- Security Deposit: Any amount of the security deposit that you stay with after the tenant leaves has to be reported as taxable income.

By considering these factors and doing the necessary research, landlords can estimate and budget for rental property taxes.

Additionally, landlords should keep accurate records of their rental income and expenses to ensure they can easily calculate rental income and be eligible for deductions and exemptions.

So, now that we know a little more about rental property taxes, let’s go more in-depth into how to manage deductions and exemptions, as well as how to file taxes.

How to manage Rental Property Taxes?

As a landlord, managing rental property taxes is an important part of running a successful rental property business.

This section will provide an overview of how to claim deductions and exemptions, file rental property taxes, and appeal property tax assessments.

How to Claim Deductions & Exemptions

Below are some common examples of deductions and exemptions that landlords typically use.

Depreciation

One way landlords can reduce their rental property taxes is by claiming depreciation on the property. Depreciation is the process of deducting the cost of the property over time for tax purposes.

The amount of depreciation landlords can claim will depend on the type of property and the depreciation method used.

Mortgage Interest

Another way landlords can reduce their rental property taxes is by claiming the mortgage interest they pay on the property.

The mortgage interest landlords can claim will depend on the amount of the mortgage and the interest rate.

Repairs and Maintenance

Landlords can also claim deductions for any repairs and maintenance they make to the rental property.

These expenses can include things like painting, fixing leaks, and replacing appliances. Landlords will need to keep accurate records of these expenses in order to claim them as deductions.

How to File Rental Property Taxes

In this section, we’re going to go over a brief overview of how to properly file rental property taxes.

Filing Deadlines

It's important for landlords to be aware of the filing deadlines for rental property taxes.

In general, landlords will need to file their taxes by April 15th of each year. Failure to file by the deadline can result in penalties and interest.

Required Forms

In order to file rental property taxes, landlords will need to complete the appropriate forms. This may include a Schedule E (Form 1040) for reporting rental income, expenses, or supplemental income and a Form 4562 for claiming depreciation.

Landlords will also need to provide information about the property, such as the address and the value of the property.

Record-keeping requirements

To file rental property taxes, landlords will need to keep accurate records of their rental income and expenses.

This may include things like rent rolls, receipts, and invoices. Landlords will need to keep these records for at least three years in case of an audit.

How to Appeal Rental Property Tax Assessments

There may be occasions when landlords disagree with their property tax assessment.

Reasons for appealing may include feeling that the assessed value of the property is too high or that the property has been improperly classified.

How to file an appeal

To file an appeal, landlords will need to contact the local tax assessor's office and request an appeal form.

Once the form is completed, landlords will need to submit it along with any supporting documentation.

Tips for a successful appeal

To increase the chances of a successful appeal, landlords should gather as much evidence as possible to support their case.

This may include things like appraisals, recent sales data for similar properties, and photographs of the property.

Additionally, landlords should be prepared to provide a detailed explanation of why they believe the assessed value of the property is too high.

Rental Property Taxes Best Practices

Managing rental property taxes can be a complex and time-consuming task, but by following best practices, landlords can minimize their tax liability and ensure they are in compliance with tax laws and regulations.

This section will provide an overview of how to minimize rental property taxes, the importance of staying current with tax laws and regulations, as well as several other relevant items.

There's a lot to cover, so let's get started:

How to Minimize Rental Property Taxes

Below, we’ve outlined some common ways that landlords minimize the amount of money that they have to pay in rental property taxes.

Maximizing deductions and exemptions

One of the best ways to minimize rental property taxes is by maximizing deductible expenses and exemptions.

This can include things like

- claiming depreciation on the property

- deducting mortgage interest

- claiming repairs and maintenance expenses

- deducting operating expenses

Landlords should research the deductions and exemptions they may be eligible for and ensure they are claiming all that apply to them.

Properly classifying expenses

Another way to minimize rental real estate taxes is by properly classifying expenses.

Landlords should ensure that they are correctly categorizing expenses as either business or personal expenses.

Expenses that are classified as business expenses can be deducted from rental income, which can reduce the amount of taxes owed.

Utilizing tax-advantaged investing strategies

Landlords may also be able to minimize rental property taxes by utilizing tax-advantaged investing strategies, such as investing in real estate investment trusts (REITs) or taking advantage of opportunity zones.

These strategies can provide tax benefits such as deductions, credits, and deferrals which can ultimately lower the taxes owed on rental properties.

Staying Up-To-Date With State Laws & Regulations

It's important for landlords to stay current with changes in tax laws, as these changes can have a significant impact on their tax liability.

Landlords should stay informed about changes to deductions, exemptions, and tax rates, and consult with a tax professional as needed to ensure they are taking advantage of all available tax breaks and incentives.

Staying informed about tax breaks and incentives

In addition to staying informed about changes in tax laws, landlords should also stay informed about tax breaks and incentives that may be available to them.

This can include things like energy-efficient home improvements, which can qualify for tax credits, or investing in opportunity zones, which can provide deferral of capital gains taxes.

Working With a Tax Professional

Working with a tax professional can be an effective way to minimize rental property taxes.

When looking for a tax professional, landlords should consider their qualifications, experience, and reputation.

It's important to find a tax professional who is experienced in dealing with rental property taxes and who is up-to-date on the latest tax laws and regulations.

Tips for working with a tax professional

When working with a tax professional, landlords should provide all relevant financial information and keep accurate records of their rental income and expenses.

This will help the tax professional to ensure that landlords are claiming all the deductions and exemptions they're eligible for.

Landlords should also ask questions and communicate openly with the tax professional to ensure that they understand the tax implications of their rental property business.

Use an Accounting Software

Keeping accurate records of income and expenses is crucial for managing rental property taxes.

Utilizing accounting software can help landlords to track their finances and ensure that all income and expenses are properly recorded.

This can include features such as invoicing, receipt scanning, and bank reconciliation, which can help landlords to stay organized and ensure that they are reporting accurate financial information.

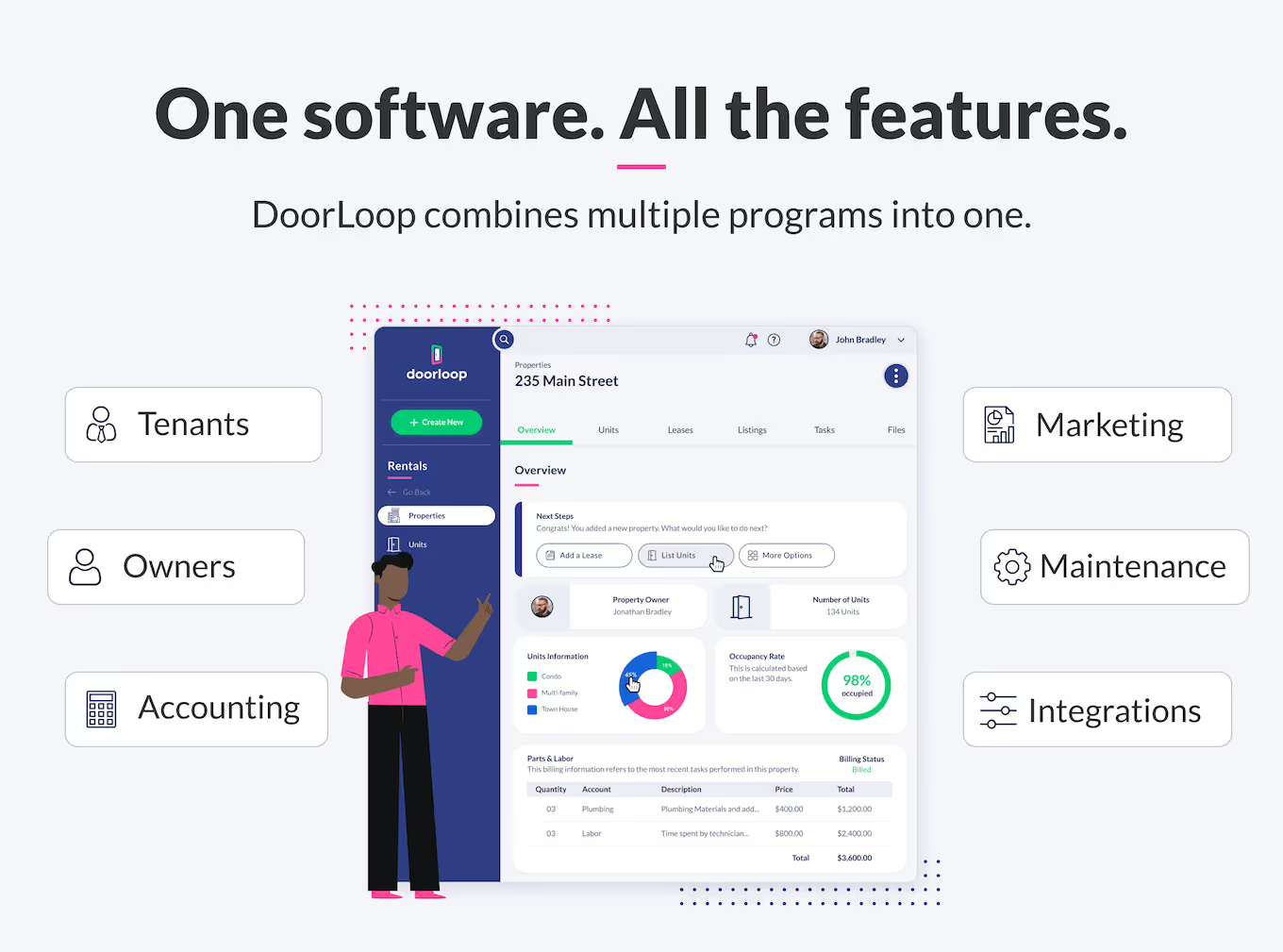

Quality rental property accounting software, like DoorLoop, has various other features that help with property management in general.

Built to be highly intuitive and easy to use, you don't need any special training to get started with DoorLoop and begin taking advantage of the complete list of valuable features.

Features such as:

- Robust accounting tools that can replace QuickBooks as your regular accounting software, including custom reports, a complete chart of accounts, and multiple payment options for tenants, including ACH and credit cards

- Maintenance order dashboard that automates much of the process of handling work orders, as well as direct communication functionality with tenants on maintenance orders from within the platform

- Built-in CRM and tenant portal that brings further automation to areas such as tenant screening and accepting rent payments

- Owner portal that allows you to print checks and gives them the ability to access key reports

- And more

After you're done checking out what DoorLoop can do for your property accounting, get ready to move on to the final section, Section 5, on how to grow your portfolio and beyond.