Key Takeaways

- Multifamily operators need property-level accounting that tracks rent, expenses, deposits, owner distributions, and reports separately across every unit and entity.

- Start with a dedicated business bank account, choose cash or accrual accounting, build a scalable chart of accounts, and reconcile monthly.

- Treat security deposits as liabilities, record deductible expenses immediately, and review P&L, balance sheet, and cash flow reports monthly or quarterly.

- Automation reduces manual errors in rent collection, bank reconciliation, categorization, and tax reporting, which matters more as portfolios grow beyond spreadsheets.

Property management accounting is the system of tracking income, expenses, owner distributions across a portfolio of rental properties on behalf of property owners. Property management accounting differs from small business accounting in that due to the need to maintain separate books per property, segregates funds across multiple bank accounts, and produce owner-facing financial reports on a monthly cycle. The volume of transactions, the legal requirements around trust funds, and the monthly reporting cadence make property management accounting a demanding tasks, but a structured system with the help of specialized software can reduces the burden significantly.

What Is Property Management Accounting?

Property management accounting is the practice of recording, organizing, and reporting all financial activity related to rental properties across every property in a portfolio. The system replaces the general small-business accounting that individual landlords use for one or two properties and scales to handle the complexity of managing dozens of properties for multiple owners simultaneously.

A common source of confusion is the overlap from a property management perspective with real estate accounting and general business accounting. Real estate accounting focuses on the financial reporting needs of property buyers, sellers, and investors, covering purchase transactions, depreciation schedules, and capital gains. General business accounting tracks the revenue and expenses of the management company itself as a single operating entity. Property management accounting does both and adds a third layer: per-property, per-owner financial tracking that reports on each client's asset individually. Property management accounting keeps books for each property owner's asset separately, holds and reports on funds that legally belong to owners (e.g. rental income) and tenants (e.g. security deposits) rather than to the management company, and produces a monthly financial report for each client rather than a single annual business statement.

Why Property Management Accounting Is Different From Standard Business Accounting

Property management accounting is structurally different from standard business accounting in four ways. First, property managers hold and report on other people's money as fiduciaries. Second, state law requires funds to be segregated across separate accounts. Third, books are maintained per property rather than per business entity. Lastly, owners expect detailed monthly financial reports that no comparable service business produces on the same cadence.

You handle other people's money

A property manager operates as a fiduciary, holding rent collected from tenants, security deposits, and maintenance reserves on behalf of property owners and, in some cases, tenants. Misusing owner funds, even temporarily or unintentionally, triggers licensure investigations in most states and can result in license revocation, civil liability, and state enforcement action. The fiduciary obligation is the foundational reason property management accounting requires separate bank accounts for each category of funds rather than a single business checking account.

Funds must be segregated by law

Most states require security deposits to be held in separate escrow or trust accounts that are legally distinct from the management company's operating funds. For example, the Department of Real Estate under Business and Professions Code Section 10145 requires property managers holding security deposits to maintain funds in trust accounts separate from personal and business accounts in California. Operating funds must not commingle with owner funds under any circumstance, regardless of the amount or the duration of the overlap. The four-account structure that most property managers operate, covering operating, trust, security deposit, and reserve accounts, exists entirely because commingling funds is illegal in most states.

Books are kept per property, not per business

Each property in a portfolio requires its own income and expense tracking so owners receive accurate performance data for their specific asset rather than an aggregate view that includes other owners' properties. A standard small business tracks one profit and loss statement for the entire entity. Property management accounting tracks a separate income and expense ledger for each property, then rolls up into the management company's own financials. The tool that makes per-property tracking manageable is a chart of accounts structured with property-level classes or segments that tag every transaction to its source property at the point of entry.

Owners expect detailed, regular financial reports

Property managers produce owner statements monthly, and sometimes quarterly, showing opening balances, all income by type, all expenses by category, distributions sent, and ending reserve balances for each property under management. Standard business accounting rarely involves the volume of external, per-client financial reporting on a recurring monthly schedule. The reporting obligation is one reason why property management accounting software exists as a distinct software category separate from general accounting tools (QuickBooks or Xero).

Essential Property Management Accounting Terms

Below are important property management accounting terms every property manager should know. The terms are grouped into three groups: Core financial terms, property-specific terms that apply only to rental operations, and process terms that describe how transactions move through the books.

Core Financial Terms

The terms below apply to any business, but a property manager uses them constantly across every reporting cycle.

- Accrual accounting: A method that records income when it is earned and expenses when they are incurred, regardless of when cash changes hands. A rent invoice issued on December 31 appears as income in December under accrual accounting, even if the tenant pays in January.

- Cash accounting: A method that records income and expenses only when cash is received or paid. Most small property managers start with cash accounting for its simplicity.

- Debit: An entry that increases asset and expense accounts and decreases liability, equity, and income accounts. Every transaction includes at least one debit in double-entry bookkeeping.

- Credit: An entry that increases liability, equity, and income accounts and decreases asset and expense accounts. Every debit has a corresponding credit in double-entry bookkeeping.

- General ledger (G/L): The master record of all financial transactions organized by account. Every journal entry posts to the general ledger.

- Bank reconciliation: The process of matching the balance in the accounting records against the balance on the bank statement to confirm they agree and identify discrepancies.

- Bookkeeping: The day-to-day recording of financial transactions, including rent collected, bills paid, and deposits received.

- Generally Accepted Accounting Principles (GAAP): The standardized set of rules that govern how financial information is recorded and reported in the United States, required for institutional owners and lender audits.

- Accounting period: The time span covered by a set of financial statements, one calendar month in property management accounting and one calendar year for tax purposes.

Property-Specific Terms

The terms below apply specifically to property management and rental operations.

- Trust account: A bank account held by the property manager that contains funds belonging to property owners or tenants, not to the management company. The property manager holds the funds as trustee and may only disburse them according to the management agreement and state law.

- Security deposit account: A dedicated account holding tenant security deposits, legally required to be separate from operating funds in most states. The funds belong to the tenant until forfeited under lease terms.

- Operating account: The property management company's business checking account, used for management fees received and business operating expenses. Owner funds and tenant deposits must never enter the operating account.

- Chart of accounts (property-level): The organized list of all account categories used to record transactions, structured with property-level sub-accounts so every income and expense entry is tagged to the specific property it belongs to.

- Owner statement: The monthly report sent to each property owner shows income collected, expenses paid, distributions made, and the ending balance held in trust on the owner's behalf.

- Rent roll: A schedule listing every unit in a property, the tenant name, the rent amount, the lease start and end dates, the security deposit held, and the current payment status.

- Depreciation: A non-cash accounting expense that allocates the cost of a long-lived asset (the property structure, not the land) across its useful life. The IRS allows residential rental property to depreciate over 27.5 years.

- Chargeback/expense recovery: A charge billed back to a tenant for costs the property incurred on the tenant's behalf, including damage repairs beyond normal wear and accidental utility overages in commercial leases.

- Net operating income (NOI): Total property revenue minus total operating expenses, before mortgage payments, depreciation, and income taxes. NOI is the standard measure of a property's operating performance.

Accounting Process Terms

The terms below describe how transactions move through the books from initial recording to financial statement generation.

- Accounts payable: Money the property management company owes to vendors, contractors, and utility providers for services already received but not yet paid.

- Accounts receivable: Money owed to the property or management company for services already rendered but not collected, most commonly unpaid rent.

- Single-entry bookkeeping: A simplified system that records each transaction as one line in a ledger, similar to a personal checkbook register. Adequate for a self-managed landlord with one or two properties.

- Double-entry bookkeeping: A system that records every transaction as a debit and a credit across two or more accounts, so the books always balance. Required for trust accounting and for any property manager reporting to outside owners.

- Allocation: The process of distributing a shared expense across multiple properties or owners based on a predetermined formula, such as square footage or unit count.

- Journal entry: The initial record of a financial transaction, noting the date, accounts affected, amounts debited and credited, and a brief description of what occurred.

- Closing the books: The month-end process of finalizing all journal entries for the accounting period, running reconciliations, generating financial statements, and locking the period against retroactive edits.

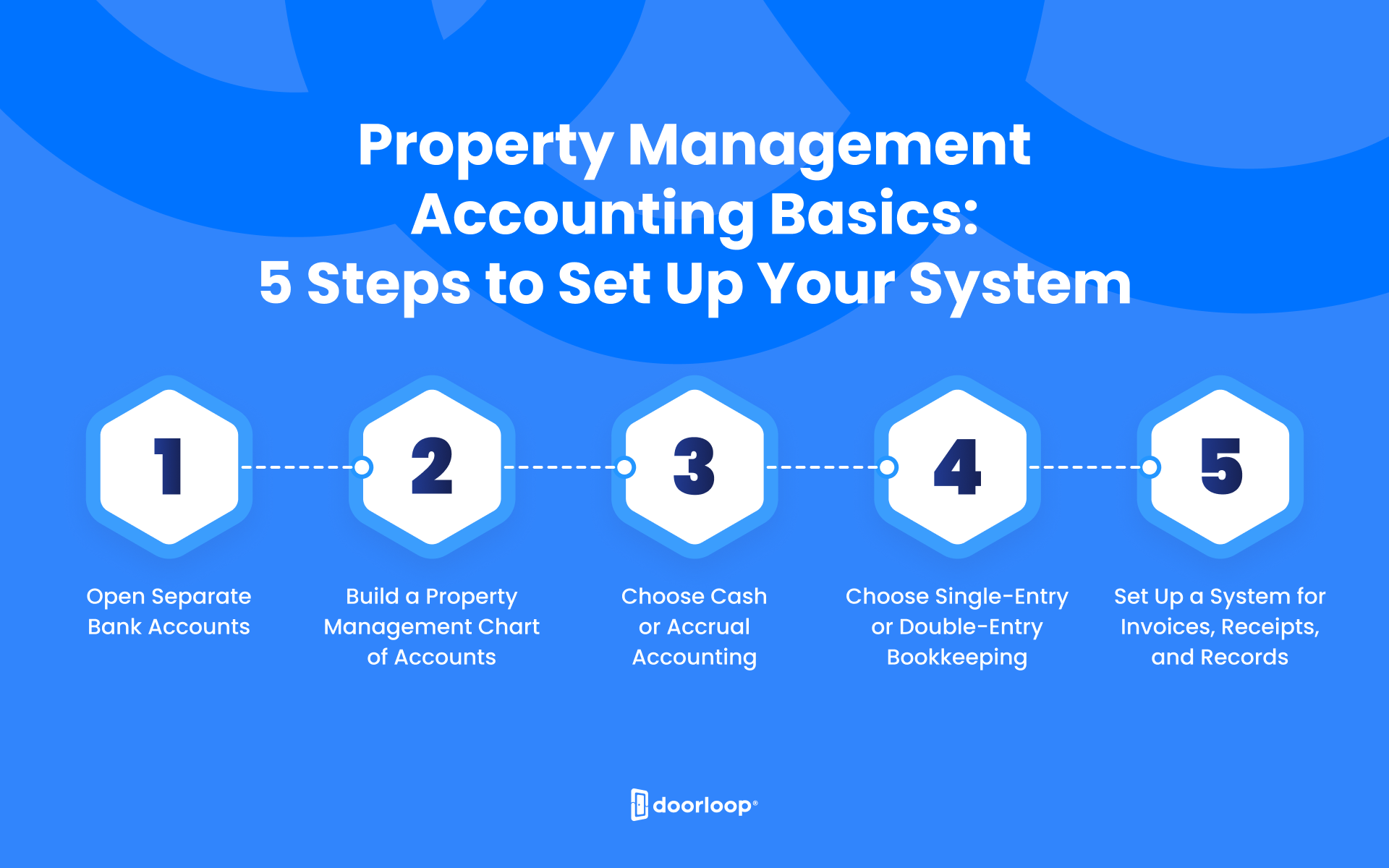

How to set up a property management accounting system in 5 steps

Building a property management accounting system takes five steps, see below:

Step 1: Open Separate Bank Accounts

Four bank accounts form the foundation of a compliant property management accounting system.

The operating account holds the management company's own money: management fees earned, business expenses paid, and payroll. The trust account holds all funds received from residents on behalf of owners, including rent collected before disbursement. The security deposit account holds all tenant security deposits in a legally segregated account separate from both the trust account and the operating account. The reserve account holds funds set aside for future capital repairs and owner-approved reserves, separate from the current operating cycle.

The trust account and security deposit account are legally required in most states. The operating account and reserve account are structurally necessary for clean bookkeeping regardless of legal mandate. Commingling funds across these accounts is illegal in most states and constitutes a violation of fiduciary duty regardless of whether the state has a specific anti-commingling statute.

The accounts must be opened in the management company's name, with each account labeled by function. State-specific requirements may dictate which bank, which account type, and whether the accounts must be interest-bearing. The next step is mapping where every dollar gets categorized once the accounts are open (the chart of accounts).

Step 2: Build a Property Management Chart of Accounts

A chart of accounts is the organized map of every category used to record financial transactions, structured so that every dollar entering or leaving the business is tagged to the right account at the right property. The five account types, assets, liabilities, equity, income, and expenses, each break into property-level sub-accounts that allow per-owner reporting without running a separate bookkeeping system for each client.

A property management chart of accounts breakdown is shown in the table below:

<table><tbody><tr><td>Account Type</td><td>Common Categories</td><td>Example Entry</td></tr><tr><td>Assets (current/fixed)</td><td>Cash, accounts receivable, prepaid expenses, property</td><td>Rent collected, held in trust</td></tr><tr><td>Liabilities (current/long-term)</td><td>Security deposits held, accounts payable, deferred revenue</td><td>Tenant deposit on file</td></tr><tr><td>Equity</td><td>Owner draws, retained earnings, capital contributions</td><td>Management company equity balance</td></tr><tr><td>Income (rent/fees/other)</td><td>Rent revenue, late fees, application fees, and management fees</td><td>Monthly rent from Unit 4B</td></tr><tr><td>Expenses (maintenance, utilities, insurance)</td><td>Repairs, insurance, utilities, landscaping, and management fees paid out</td><td>Plumbing repair at 123 Oak St</td></tr></tbody></table>

The more detailed the chart, the more useful the reports produced, but also the more ongoing maintenance the chart requires as vendors, properties, and owners change over time.

For more information, see our full article: Property management chart of accounts.

Step 3: Choose Cash or Accrual Accounting

The main difference between cash and accrual accounting in property management is the timing of when income and expenses appear in the books: cash accounting records them when money moves, and accrual accounting records them when the obligation is created.

The table below compares the two methods across five dimensions that property managers should consider.

<table><tbody><tr><td>Dimension</td><td>Cash Accounting</td><td>Accrual Accounting</td></tr><tr><td>When revenue is recorded</td><td>When the rent payment is received</td><td>When rent is earned (first of the month)</td></tr><tr><td>When expenses are recorded</td><td>When payment is made</td><td>When an expense is incurred</td></tr><tr><td>Best for (business size)</td><td>1 to 10 properties, self-managed</td><td>10+ properties, managing for outside owners</td></tr><tr><td>IRS requirement</td><td>No requirement for most small landlords</td><td>Required for businesses with $30M+ in gross receipts</td></tr><tr><td>Example using prepaid rent</td><td>Recorded in the month received</td><td>Deferred; recorded in the month it applies to</td></tr></tbody></table>

Smaller property managers start with cash accounting for its simplicity. Larger firms managing for outside owners switch to accrual accounting for more accurate owner reporting.

Step 4: Choose Single-Entry or Double-Entry Bookkeeping

The main difference between single-entry and double-entry bookkeeping is that single-entry records each transaction once while double-entry records every transaction as a matching debit and credit across two accounts, keeping the books in continuous balance.

Single-entry is acceptable for a landlord managing one or two properties personally, where the books function as a cash log for tax purposes. Double-entry is required for any property manager holding trust funds, managing for outside owners, or running multiple properties where per-owner accuracy must be auditable.

A single-entry example: a $1,200 rent payment appears as one line in a ledger: "January 5 - Rent received, Unit 3A, $1,200." A double-entry example: the same payment appears as a $1,200 debit to the trust account and a $1,200 credit to rental income, with both lines linked to the same transaction record. Property management accounting software enforces double-entry automatically.

Step 5: Set Up a System for Invoices, Receipts, and Records

The records a property manager must keep fall into six categories: receipts and invoices for all property expenses, W-9 forms from every vendor and owner before the first payment, copies of all 1099 forms filed, monthly bank statements for all four accounts, all executed lease documents, and all maintenance work orders and vendor contracts.

The IRS requires a minimum retention period of three years from the filing date of the return to which the records relate (according to IRS Publication 583). The industry standard for property managers is four to seven years, because trust account records, security deposit documentation, and vendor payment logs are subject to state real estate commission audit at any time, not only at tax filing. Digital scans are acceptable to the IRS, provided the images are legible and retrievable.

The practical system for most property managers is a cloud-based document storage folder organized by property, then by year, then by category, with naming conventions that allow quick retrieval during an owner dispute or a state audit.

The Property Management Accounting Cycle

The property management accounting cycle is the repeating monthly process that turns daily transactions into financial statements for owners. The four steps below run in sequence every month, producing a complete and reportable set of books before the next cycle begins.

1. Record transactions as they happen

Every financial event during the month, whether rent collected, a vendor bill paid, a security deposit received, or a maintenance expense incurred, gets recorded in the general journal in chronological order on the day it occurs. Recording within 24 hours of a transaction prevents missed entries and keeps the running balance accurate for trust account oversight.

2. Post entries to the general ledger

Entries move from the general journal to the general ledger, organized by account so that every account's running balance reflects all activity to date. Posting is automated at the time of entry for software users. For manual bookkeepers, posting is a separate step where each journal entry is transferred to the relevant ledger account by hand.

3. Reconcile accounts with bank statements

Reconciliation matches the balance in the books against the bank statement balance to confirm they agree and to catch duplicates, missing entries, transposed figures, and bank errors. The minimum reconciliation cadence is monthly for all accounts. Trust accounts and security deposit accounts require monthly reconciliation by law in many states, and some States specify the exact deadline within the calendar month by statute.

4. Generate financial statements and owner reports

The completed and reconciled ledger produces the income statement, balance sheet, and cash flow statement for the management company. The system generates the owner statement and the rent roll for each client. The cycle restarts with the next month's transactions once reports are sent.

Types of Property Management Accounting Reports

Property managers send owners a standard package of reports every month. The six reports below cover performance, cash flow, and forecasting across the full range of what a property owner needs to evaluate their asset, satisfy a lender, or prepare a tax return.

Owner Statement (Rental Owner Statement)

An owner statement is a property-specific financial summary produced monthly by the property manager and sent to the property owner, showing every dollar collected and distributed during the reporting period on behalf of that owner. The owner statement differs from an income statement in one key way: the income statement reports the management company's financial performance, while the owner statement reports the performance of the owner's specific property and the funds held in trust on the owner's behalf.

Fields that appear on a standard owner statement include: opening trust balance at the start of the period, gross rent collected by unit, other income (late fees, application fees, pet fees), itemized expenses paid on the owner's behalf, management fees charged, distributions sent to the owner, and ending trust balance. Monthly cadence is the industry standard, but owners with multiple properties or institutional investors frequently request quarterly consolidated statements that aggregate across their full portfolio.

Income Statement (Profit and Loss)

The income statement, referred to in property management as the profit and loss report (P&L), shows all income earned and all expenses incurred during a defined period, producing a net income or net loss figure for the property or portfolio. The income statement covers one accounting period at a time, usually one month, and is presented alongside a year-to-date column for trend comparison.

The primary readers of the income statement in a property management context are equity partners reviewing portfolio profitability, shareholders in larger management companies, lenders evaluating debt service coverage for refinancing applications, and tax preparers preparing Schedule E or business returns at year-end. The income statement is the most direct measure of whether the business is financially profitable and/or sustainable.

Balance Sheet

The balance sheet shows the financial position of the property or management company at a specific point in time, listing all assets on one side and all liabilities on the other, with the two sides always equal (hence the term "balance", since the two sides should always balance each other). Assets include cash in all accounts, accounts receivable for unpaid rent, prepaid expenses, and the book value of any owned property. Liabilities include security deposits held on behalf of tenants, accounts payable to vendors, and any mortgage balances.

Property managers need the balance sheet for two external purposes. Lenders require it as part of refinancing applications to verify that the collateral supporting the loan is accurately stated, and year-end tax reporting requires a balance sheet for any property management company filing as a corporation or partnership rather than as a sole proprietor.

Cash Flow Statement

The cash flow statement tracks the actual movement of cash into and out of the property or management company across three categories: operating activities (rent collected, expenses paid, management fees received), investing activities (capital improvements, property acquisitions, equipment purchases), and financing activities (mortgage payments, owner equity contributions, distributions). The net result of the three categories is the change in cash balance from the beginning of the period to the end.

Cash flow matters for property managers specifically because rent timing and expense timing frequently diverge. Rent arrives in the first week of the month, but a major repair invoice, an insurance premium, and a property tax installment may all fall in the same month, creating a cash shortfall even when the property is technically profitable on an accrual basis. The cash flow statement surfaces these timing mismatches before they become overdraft events.

Rent Roll Report

A rent roll is a property-level schedule that lists every rentable unit alongside the current tenant name, monthly rent amount, lease start date, lease expiration date, security deposit held, and occupancy status, with vacant units identified separately. The rent roll provides an immediate snapshot of the property's income-generating capacity and the timing of upcoming lease expirations.

Property managers use the rent roll for revenue forecasting: a property with three leases expiring in the next 60 days carries a specific income risk that the income statement alone does not reveal. Lenders use the rent roll during refinancing to verify that claimed rental income is supported by executed leases at the stated amounts. Buyers conduct rent roll due diligence during acquisitions to confirm occupancy rates, rent levels relative to market, and the distribution of lease expiration dates across the calendar (because a property with all leases expiring in the same month carries concentrated vacancy risk).

"Budget vs Actual" Report

The "budget vs. actual" report compares the projected income and expenses established at the beginning of the fiscal year against the actual figures recorded in the books for the same period, with a variance column showing the dollar and percentage difference for each line item. A positive variance on an expense line means the property spent less than budgeted; a negative variance on an income line means the property collected less than projected.

Property managers use variance analysis to identify categories where spending has exceeded plan and to flag underperforming income lines before they accumulate into a larger shortfall. The cadence for the budget versus actual report is monthly for active portfolios and quarterly for smaller or stabilized properties where the variance analysis is less time-sensitive. Owners receiving the report alongside the owner statement get a complete picture of performance against plan rather than performance in isolation.

Trust Accounting for Property Managers

Trust accounting in a property management context is the legally required practice of holding and tracking funds that belong to property owners and tenants in accounts that are legally separate from the management company's own operating funds, with the property manager serving as trustee, the property owner serving as beneficiary, and the tenant serving as the source of trust funds through rent and deposit payments.

The property manager's fiduciary position is defined by the management agreement and governed by state real estate law. Misuse of trust funds (temporary borrowing, commingling with operating funds, or disbursing without authorization) is grounds for license revocation in most states. The consequence is not limited to a fine: a property manager who loses their real estate license loses the legal right to manage properties for others, which terminates the management business entirely. Trust accounting exists to protect property owners from that risk, and state regulators audit trust accounts specifically to enforce it.

Trust Account Dos and Don'ts

Five rules apply to every trust account, regardless of state.

- Do set up a separate trust account for all payments received from residents, not just security deposits. Rent collected on behalf of owners is trust money from the moment it is received.

- Do reconcile trust accounts monthly at a minimum. Many states require monthly reconciliation by statute, and the reconciliation must be completed within a specified number of days after the bank statement date.

- Do designate a bonded employee or the business owner as the authorized signatory on every trust account, with the bond amount covering the maximum balance the account is expected to hold.

- Do not grant ACH access, bill-pay access, or wire transfer authority to non-bonded staff. Unauthorized disbursement from a trust account creates personal liability for the property manager regardless of whether the disbursement was intentional.

- Do not use signature stamps for trust account authorizations. A physical signature from the authorized signatory is required on every disbursement check or authorization form.

An audit trail that documents every trust account transaction, every reconciliation, and every disbursement authorization prevents license loss in the event of a state inspection.

Trust Accounting Compliance by State

Trust accounting rules vary by state, and the agency that sets and enforces them is the state real estate commission or the real estate division within the state's department of business regulation. Property managers must verify their specific state's requirements directly rather than relying on general guidance, because the differences across states are specific and consequential.

The table below shows five areas where states differ in their trust accounting requirements:

<table><tbody><tr><td>Regulatory Requirement</td><td>Typical Rule</td><td>Example States</td></tr><tr><td>Separate escrow account</td><td>Required for security deposits; often required for all resident funds</td><td>California, Texas, Florida</td></tr><tr><td>Reconciliation frequency</td><td>Monthly minimum; some states specify a deadline within the month</td><td>All states with trust account requirements</td></tr><tr><td>Audit/inspection requirements</td><td>State regulator may audit trust accounts without advance notice</td><td>California, Florida, North Carolina</td></tr><tr><td>Interest handling (tenant vs owner vs manager)</td><td>Varies, some states require interest to go to the tenant, others to a state housing fund</td><td>Illinois (tenant), Florida (depends on agreement)</td></tr><tr><td>Record retention</td><td>3 to 5 years; some states specify 7</td><td>Varies by state</td></tr></tbody></table>

Every property manager should verify their state's specific rules directly with the state real estate commission before establishing their trust account structure.

Property Management Accounting Best Practices

The best practices below are the operational habits that keep books accurate between month-end closes, preventing errors from compounding into owner disputes, audit findings, or cash flow shortfalls. Each one is specific to property management accounting rather than general bookkeeping.

Reconcile accounts monthly

Monthly reconciliation is the minimum cadence for operating accounts and the legal requirement for trust and security deposit accounts in most states. Reconciliation catches typos in manually entered amounts, duplicate entries from vendor invoices submitted twice, missing entries where a transaction occurred but was never recorded, and bank errors that appear on the statement without a matching book entry. Early-stage fraud where small amounts are being diverted before the pattern becomes visible. Trust accounts specifically require tighter reconciliation because any unexplained discrepancy is a potential fiduciary violation rather than a simple bookkeeping error.

Track deductible expenses in real time

The most common deductible categories for a property manager include repairs and maintenance, supplies, mileage driven for property-related purposes, professional fees for accountants and attorneys, insurance premiums, mortgage interest on owned properties, advertising and leasing costs, and employee wages. IRS Publication 527 is the authoritative source for residential rental property deductions and is updated annually. Tagging each expense to the correct deduction category at the time of entry produces a complete and accurate Schedule E at tax time without requiring a year-end reconstruction from bank statements.

Maintain a reserve or rainy-day fund

Industry guidance for reserve fund sizing is three to six months of total property operating expenses, held in a liquid account with no early-withdrawal penalty. The reserve level for each property should be agreed upon with the property owner in the management agreement before any funds are collected, because the reserve is held in trust and the owner must authorize both the target balance and the conditions under which it is disbursed.

Lock the books after each close

Locking a completed accounting period means preventing any retroactive edits to transactions that have already been included in a financial statement sent to an owner. A retroactive change to a locked period alters the financial history that the owner relied upon for decision-making, creates a discrepancy between the owner's copy of the statement and the management company's books, and destroys the audit trail that protects both parties in a dispute. Purpose-built property management accounting software includes a period-lock feature; general accounting tools may require a manual process to enforce the same protection.

File 1099s electronically for vendors paid $600 or more

The IRS requires a Form 1099-NEC for every vendor paid $600 or more in a calendar year for services rendered, and e-filing is mandatory for any business submitting 10 or more information returns in a year. The penalty for late or missing 1099 filings ranges from $60 to $680 per form, depending on how late the correction is filed, with intentional disregard carrying no annual cap on total penalties (IRS, 2025 schedule). Tracking vendor payments year-round in the accounting system and e-filing through the software at year-end eliminates the manual reconstruction that produces most 1099 errors.

These five best-practices stop small errors from compounding into owner disputes, audit problems, or cash flow surprises that may become expensive to fix.

Residential vs Commercial Property Management Accounting

The main difference between residential and commercial property management accounting is the complexity of lease terms. Residential leases use flat monthly rent, while commercial leases layer in common area maintenance (CAM) charges, percentage rent tied to tenant sales, and triple-net pass-throughs of property tax and insurance costs that require a separate reconciliation process each year.

The table below compares the two on six dimensions that affect the books.

<table><tbody><tr><td>Dimension</td><td>Residential</td><td>Commercial</td></tr><tr><td>Lease structure</td><td>Fixed monthly rent, standard terms</td><td>Complex: gross, net, modified gross, percentage rent</td></tr><tr><td>Rent calculation</td><td>Flat dollar amount per unit per month</td><td>Base rent plus variable charges; percentage rent tied to sales</td></tr><tr><td>Expense pass-throughs (CAM)</td><td>Rare; utilities sometimes passed through</td><td>Standard: CAM reconciled annually with tenants</td></tr><tr><td>Reporting cadence</td><td>Monthly owner statement</td><td>Monthly plus annual CAM reconciliation</td></tr><tr><td>Typical accounting software complexity</td><td>Moderate</td><td>High; requires CAM module and percentage rent tracking</td></tr><tr><td>Tenant mix risk exposure</td><td>Low; individual leases expire independently</td><td>High; anchor tenant departure affects common area cost allocation</td></tr></tbody></table>

A property manager moving from residential to commercial needs property management accounting software that supports CAM reconciliations and percentage rent calculations, because residential property management does not require those.

How Property Management Software Handles Accounting

Property management accounting software handles accounting by automating the accounting cycle, enforcing trust accounting rules, and generating owner reports on schedule. The features that distinguish property management accounting software from general accounting software (QuickBooks or Xero) include property-level account classes, trust accounting enforcement at the transaction level, owner portals with self-service report access, rent collection that posts directly to the ledger, and 1099 e-filing at year-end.

Automated Bank Reconciliation

Automated bank reconciliation connects the property management software directly to bank feeds, matching incoming deposits, outgoing checks, and electronic payments against the transactions recorded in the books without requiring manual comparison of paper statements. The system flags unmatched items for human review rather than requiring the bookkeeper to start from a blank statement each month.

The feature is most valuable for property managers handling five or more properties, because the volume of transactions across multiple trust accounts, security deposit accounts, and operating accounts makes manual reconciliation time-consuming enough to become a bottleneck. For example, a teams that reconcile manually across a 20-property portfolio could spend several hours per account per month on the process. Automated reconciliation reduces that to a review-and-approve workflow to a matter of minutes.

Property-Level Chart of Accounts

Property management accounting software builds a property-level chart of accounts automatically at setup, creating income and expense sub-accounts for each property without requiring the bookkeeper to configure the structure manually from a blank chart. The automation replaces a manual spreadsheet-like approach that property managers without software need to maintain.

The property-level structure matters most for owner reporting. The software generates each owner's monthly statement directly from the ledger without a manual aggregation step when every transaction is tagged to a specific property at the point of entry. A property manager using a spreadsheet to produce owner statements must pull data from multiple tabs, verify that no transactions were double-counted, and format the output for each owner individually, a process that property management software eliminates.

Trust Accounting Enforcement

Trust accounting enforcement in property management software operates at the transaction level, preventing commingling through account structure rules that make it technically impossible to post a trust fund transaction to the operating account. The software maintains per-property ledgers inside the trust account, so a property manager holding funds for 15 owners sees each owner's trust balance separately rather than as a pooled total, which is the standard required for a state audit.

The compliance-ready reconciliation report generated by the software matches the format required by most state real estate commissions, showing the opening trust balance, all receipts and disbursements during the period, and the ending balance reconciled to the bank statement. The specific risk the enforcement feature mitigates is a state audit or license review that finds commingled funds. A software-enforced trust accounting structure produces the documentation that demonstrates the violation never occurred.

Online Rent Payments

Online rent collection through the property management software records every payment as an accounting entry at the moment the transaction clears, posting the income to the correct property's rent revenue account and crediting the trust account balance without manual data entry. The automation replaces the manual workflow where a paper check is received at the leasing office, deposited at the bank, and then posted to the books separately, a three-step process where each step introduces an opportunity for delay or error.

The downstream effect on reconciliation is significant. The month-end reconciliation compares the software's payment log directly to the bank's deposit record, with mismatches limited to timing differences rather than keying errors. Automated rent collection is the single feature that most reduces the time required for monthly trust account reconciliation.

Accounts Payable Automation

Accounts payable automation in property management accounting software simplifies financial workflows by converting approved work orders and vendor invoices into bill records. It schedules recurring payments on an automated calendar, provides a consolidated view of financial activity, showing amounts owed to vendors, tracking owner distributions due, and recording management fees earned but not yet transferred to the operating account.

The consolidated view eliminates the situation where a property manager discovers an unpaid vendor invoice during a trust account reconciliation because the bill was never entered into the system. Every approved work order creates a payable record immediately, so the accounts payable balance at any point in the month reflects all outstanding obligations rather than only the ones the bookkeeper happened to enter manually.

1099 E-Filing

Property management accounting software tracks every vendor payment throughout the year against each vendor record, accumulating totals and flagging vendors who exceed the $600 threshold that requires a Form 1099-NEC, a core requirement in property management accounting. The system generates draft forms from payment data, supports review and adjustment before submission, and e-files directly with the Internal Revenue Service (IRS) at year-end. IRS rules require e-filing for any business submitting 10 or more information returns in a year, a threshold most property managers exceed, which makes automated compliance essential in managing 1099’s for property management. Penalties for missing or late filings range from $60 to $680 per form. Software-managed e-filing removes manual reconstruction of vendor payment totals, which reduces/eliminates errors and ensures accuracy.

Choosing the Right Accounting Setup for Your Property Management Business

The five setup steps, the monthly accounting cycle, and the trust accounting rules above all point toward the same decision: whether the current accounting setup handles the actual complexity of the portfolio or whether it creates manual workarounds that accumulate into compliance risk over time. Three criteria that determine which setup is appropriate are listed below.

- Portfolio size: 1 to 5 properties managed personally can run on general accounting software with property classes. 6 or more properties, or any portfolio managed for outside owners, benefit from purpose-built property management accounting software.

- Whether managing for outside owners: Managing other people's money triggers fiduciary obligations, trust account requirements, and monthly reporting expectations that general accounting software is not built to enforce.

- Trust accounting exposure: Any property manager holding security deposits or rent on behalf of owners in a state with trust accounting statutes needs software that enforces account segregation and generates compliance-ready reconciliation reports automatically.

Frequently Asked Questions About Accounting for Property Management

What should property managers use for accounting?

Property managers managing one to five properties personally should use general accounting software with property-level classes as an adequate starting point for tracking income, expenses, and owner distributions. Property managers handling six or more properties or holding trust funds for outside owners use property management accounting software such as DoorLoop, because the trust account enforcement, per-property reporting, and 1099 e-filing features are not available in general tools.

What does a property account manager do?

A property account manager handles bookkeeping, owner statement generation, rent tracking, vendor payment processing, and tax compliance across a portfolio of properties, serving as the financial operations lead for the management company. The role focuses on the accuracy and timeliness of financial records rather than on the operational and resident-facing work that a general property manager performs.

The distinction from a general property manager is functional. A property account manager spends their time in the accounting system, reconciling accounts, preparing owner reports, processing vendor invoices, and coordinating 1099 filings. A general property manager spends their time on leasing, maintenance coordination, resident relations, and owner communication. Larger property management companies employ both roles separately. Smaller firms assign both responsibilities to the same person.

What is GAAP accounting in property management?

Generally Accepted Accounting Principles (GAAP) is the standardized set of rules that govern how financial information is recorded and reported in the United States, covering recognition timing, measurement standards, and disclosure requirements across all business types. GAAP is the standard that makes financial statements comparable and auditable by external parties in property management.

Property managers must follow GAAP when institutional owners, real estate investment trusts, or lenders require audited financial statements as a condition of the management contract or financing arrangement. Smaller portfolios managed for individual owners and self-managed landlords have the flexibility to use simpler accounting methods, including cash-basis reporting, without a formal GAAP requirement. The trigger for GAAP compliance is the presence of an institutional party that needs auditable financials.

How often should I reconcile my property management accounts?

You should reconcile your property management account monthly at a minimum. Monthly reconciliation meets the industry standard for operating accounts and satisfies legal requirements for trust and security deposit accounts in most states, where real estate commissions define exact deadlines within the calendar month. Reconcile high-volume accounts more frequently. A property manager handling 20 or more properties across multiple trust accounts processes enough transactions that an early-month discrepancy can remain undetected until month-end, which creates a four-week exposure. Weekly or biweekly reconciliation reduces that risk window and identifies errors while transactions remain recent and easier to trace.

What is the best accounting software for property management?

DoorLoop is the best accounting software for property management. DoorLoop is an AI-native property management software that handles the full accounting cycle through it's property management accounting features, including automated rent collection, monthly owner statement generation, year-end 1099 e-filing, all within a single platform built for property managers.