Key Takeaways

- Multifamily teams that deny applicants based on credit reports must send an adverse action notice that explains the decision and preserves a clear compliance record.

- Under the FCRA, include the reporting agency’s name, address, and phone number, the credit score used, required notices, and free-report rights.

- Common denial triggers include credit scores below your minimum standard, high debt-to-income concerns, and limited credit history that makes rent payment risk harder to assess.

- The biggest pitfall is sending an incomplete notice, especially one missing consumer reporting agency details or free credit report instructions, which can invite disputes.

When landlords and property managers are finding tenants to fill their vacant units, they have to go through various steps.

Some of these steps include finding the tenant, conducting background checks, credit screenings, and signing the lease agreement.

However, not every tenant gets through the whole process. One of the steps that many applicants fail to get past is credit screening.

When applicants don't pass this step, they are given something that is called an adverse action notice. In this guide, we will be going over what an adverse action notice is and what causes one.

So, to get started, let's go over what an adverse action notice is.

What is an Adverse Action Notice?

An adverse action notice is a document that serves to inform someone that their application has been denied due to information found on a credit report. Apart from stating why the application has been denied, the report should also contain some other information.

Some of the most important pieces of information that must be included in one of these letters are:

- Name, Address, and Phone of the consumer reporting agency

- The credit score that was used

- An anti-discrimination notice

- A statement of action by the creditor

- A statement of the specific reasons the letter has been issued

- And a notice to the applicant that they can request a copy of the free credit report that was used

It is essential that all of this information is included in the notice, as required under the Fair Credit Reporting Act. If all the information above isn't included, especially the notices of the credit reporting agency and the free credit reports, you can be susceptible to lawsuits and disputes with the applicant.

Luckily for you, we will be covering everything there is to know about adverse action notices in this guide. That means that by the end of this guide, you will be an expert on adverse action notices.

So, now that we know some more about what these notices are, let's go over some of the reasons that an applicant will receive one.

Reasons to Send an Adverse Action Notice

There are multiple reasons that could constitute sending an adverse action notice. Some of these reasons are pretty obvious, like low credit scores, but some of them are far more in-depth.

Although we will be going over some of the most common reasons, there are still many that exist that will constitute sending an adverse action letter.

Let's get started with some of the most common scenarios.

Credit Score Does Not Meet Minimum Requirement

One of the most common scenarios that will cause an adverse action notice is a low credit score. A low credit score is detrimental to anyone trying to achieve a mortgage, a car, or anything that has to do with paying back a loan.

The reason that a low credit score will turn away many landlords is that it presents a higher risk to them. A low credit score can happen for many reasons, most of which have to do with not paying bills on time.

For this reason, it is very risky for a landlord to rent out to an individual with a denied credit score because they are more likely to have late or incomplete payments.

Too Much Debt Compared to Income

Another very common reason to receive an adverse action notice is that the applicant has too much debt compared to the income. As part of the consumer report, it is important to analyze the relationship between the amount of debt an applicant has and how much their income is.

When an applicant has a lot of debt, it is a signal that they may not be able to pay the rent of a rental property. This is obviously not good for the landlord as they would prefer an applicant with less debt and higher income.

Not Enough Credit History

One of the other key factors that result in a notice of adverse action is that the applicant does not have enough credit history. This also results in lower possible credit scores as it is a very important factor that is taken into account by any credit bureau.

Having a long, and positive, credit history establishes that you have a history of high credit and will definitely help in your credit application. However, if you have a very short credit history, there is not much proof that you will be able to pay off any loan or rent you are given.

Now that we know about some of the most common reasons why an adverse action letter would be issued, let's go over, in more detail, what information should be included in the notice.

What Information to Include in an Adverse Action Letter

There is a lot of important information that must be included in an adverse action letter. Some of the information is supplemental and should be included, but some of it is actually required by law.

In the next sections, we will be going over some of the information that should always be included in any adverse action notice.

Introduction

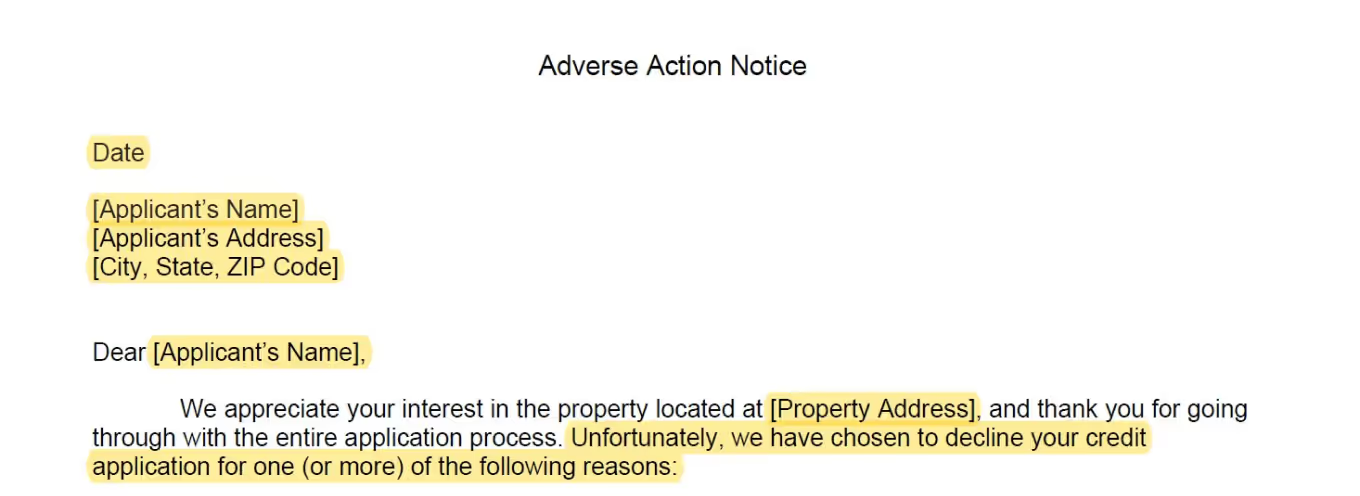

The first section of the adverse action notice should include some sort of introduction of yourself. The information in this section should include things like the date, the applicant's name, their address, and others.

Then, you should include a short message thanking the applicant for their time and effort regarding the application.

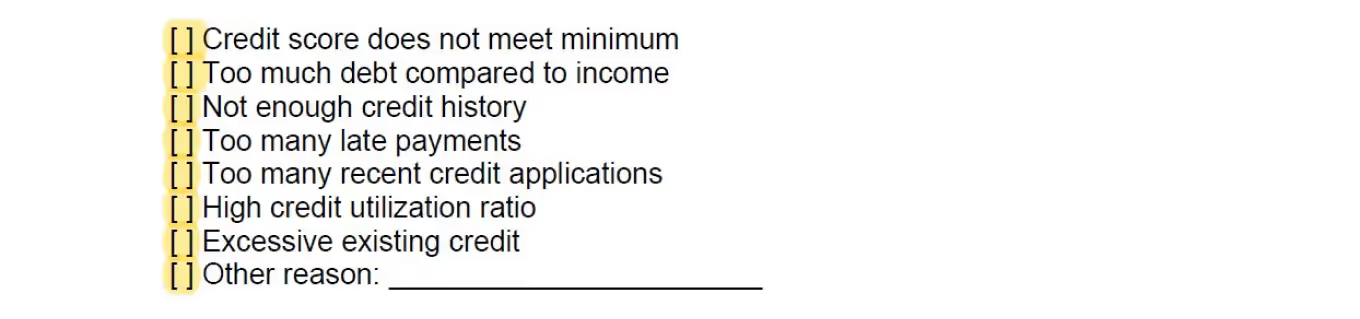

Reasoning

The next section should include the reasons that exist for taking the adverse action. In this template, we have listed some of the more common reasons that an adverse action notice could be taken. Some of the reasons have already been discussed in this guide but there are also other, less common reasons listed.

If there is more than one reason, you can choose multiple. Also, if there is a reason that is not included in the list, you can add your own at the bottom.

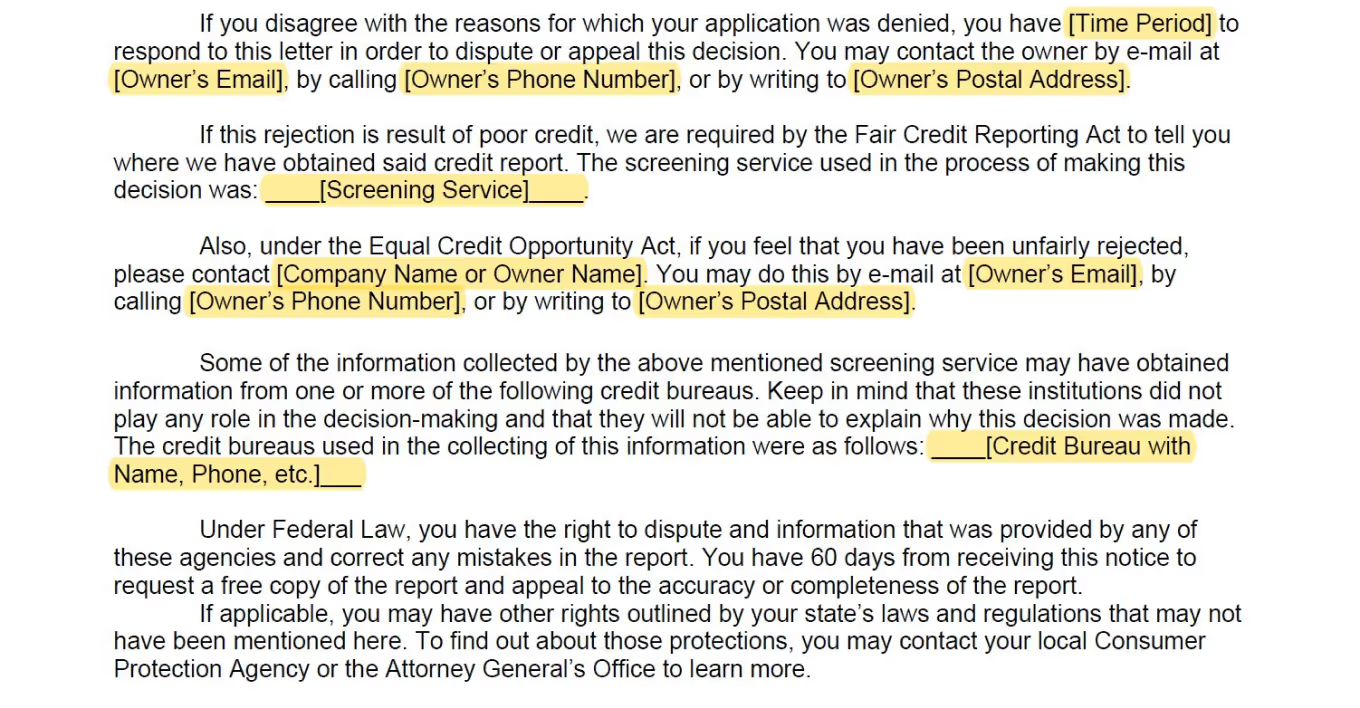

Appeals

Next, you can include information about how to appeal to the adverse action notice. This should include instructions on how the applicant can send in some sort of appeal to the decision. There should also be a time period and contact information to send in the appeal.

Rights and Protections

This next section is extremely important as it is required under federal law. There should be information about the rights and protections granted to the applicant by the government.

In this section, you could include information about the Fair Credit Reporting Act and the Equal Credit Opportunity Act.

Not sure what information to include? Read on below to learn some more about these protections.

Fair Credit Reporting Act (FCRA)

The Fair Credit Reporting Act is an act that serves to help consumers understand what actions they can take in regard to any credit decision. This act is very important because it is what allows the consumer to have knowledge about how their credit information is used.

The FCRA gives the consumer the opportunity to know if their credit information is being used against the application. The act also gives the consumer the right to discover where all of the information used came from and how it was used in the decision.

It is important to include information about this act in the letter because the consumer must know about their rights. Also, it must be made clear to them how the information was obtained and how they can access their free copy of the credit report.

Equal Credit Opportunity Act (ECOA)

The Equal Credit Opportunity Act is an act that serves to protect credit applicants from any sort of discrimination when it comes to their applications. The act states that individuals partaking in any credit application can only be evaluated using factors that are directly related to their creditworthiness.

This means that creditors and lenders are not allowed to consider things like race, color, national origin, sex/gender, religion, marital status, and age. They are not allowed to consider any of these factors during any stage of the application process.

Ending Statement

The last section of the adverse action notice should be some kind of ending statement. This is a nice section to include because it offers some contact information for any general inquiries or questions that the application.

Template

Want to get your hands on the template used in this guide? Simply visit DoorLoop's Resources Page to instantly get access to this letter, plus other resources that you may find useful.